Introduction:

- The Carbon Border Adjustment Mechanism (CBAM) introduced by the European Union from January 1, 2026, is a carbon-pricing tool that imposes a levy on imports based on their embedded emissions, aligning them with the EU’s internal carbon costs under the EU Emissions Trading System (ETS). While framed as a measure to prevent carbon leakage and ensure a “level playing field,” it has raised concerns regarding climate justice, particularly for developing economies like India.

- At a time when global climate frameworks emphasise “common but differentiated responsibilities (CBDR)”, developing countries contribute far less to cumulative emissions—India accounts for about 7% of global emissions with per capita emissions significantly below developed nations—yet face disproportionate adjustment pressures under CBAM.

- The 2026 India-EU Free Trade Agreement (FTA), which does not exempt India from CBAM but provides limited procedural engagement, sharpens this debate.

Body:

1. Structural Asymmetries and Unequal Burden-Sharing

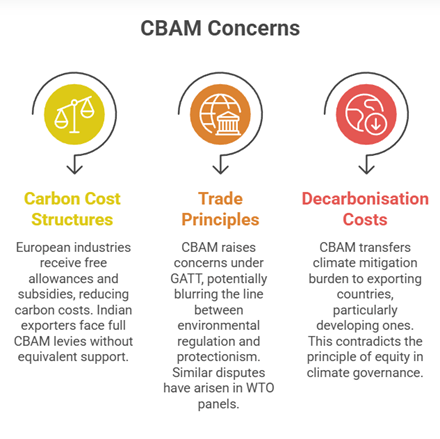

(a) Differential Carbon Cost Structures

- European industries continue to receive free allowances under ETS (phasing out 2026–2034) and substantial state subsidies for decarbonisation, reducing their effective carbon costs.

- Indian exporters in sectors like steel, aluminium, and cement face the full CBAM levy without equivalent fiscal support, creating an uneven competitive landscape.

- Example: European steelmakers benefit from green subsidies under EU Green Deal, whereas Indian firms rely largely on market financing.

(b) Tension with Multilateral Trade Principles

- CBAM raises concerns under General Agreement on Tariffs and Trade, which prohibits internal measures that indirectly protect domestic industries.

- By combining internal carbon pricing with border taxes, the EU risks blurring the line between environmental regulation and disguised protectionism.

- Case Study: Similar disputes have arisen in WTO panels over environmental standards acting as trade barriers, such as the US Shrimp-Turtle case, highlighting interpretational complexities.

(c) Shifting Decarbonisation Costs to the Global South

- CBAM effectively transfers part of the EU’s climate mitigation burden onto exporting countries, particularly developing ones lacking technological and financial capacity.

- This contradicts the principle of equity in climate governance, where developed countries are expected to lead in both mitigation and financial support.

- Example: African and Asian exporters have flagged concerns that CBAM could reduce their export competitiveness by 20–30% in carbon-intensive sectors.

2. Climate Justice and Sovereignty Concerns

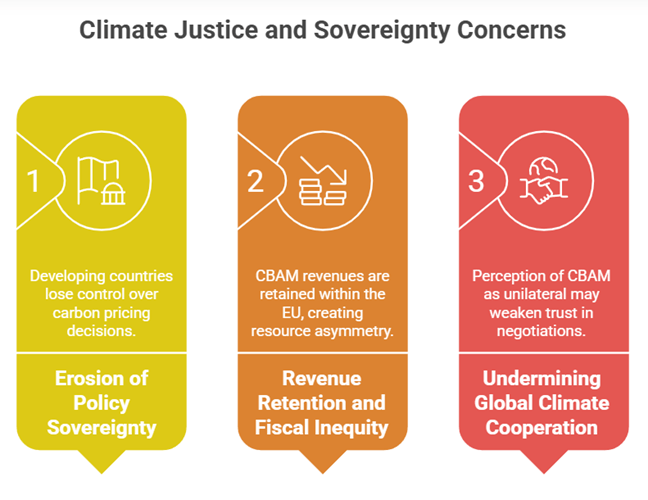

(a) Erosion of Policy Sovereignty

- Developing countries lose control over carbon pricing decisions when external regimes determine the cost of their exports.

- Without influence over CBAM rates or methodologies, countries risk becoming “rule-takers” in global climate governance.

- Example: India’s domestic carbon pricing trajectory under the Carbon Credit Trading Scheme (CCTS) may not align with EU benchmarks, limiting policy autonomy.

(b) Revenue Retention and Fiscal Inequity

- CBAM revenues are retained within the EU, despite being generated from emissions embedded in goods produced elsewhere.

- This creates a resource asymmetry, as funds that could support green transitions in developing countries are instead used in developed economies.

- Case Study: Estimates suggest CBAM could generate billions of euros annually, yet no formal redistribution mechanism exists for affected exporters.

(c) Undermining Global Climate Cooperation

- Perception of CBAM as unilateral and exclusionary may weaken trust in multilateral climate negotiations.

- It risks fragmenting global efforts by encouraging carbon clubs rather than inclusive frameworks under institutions like the United Nations Framework Convention on Climate Change.

- Example: Several developing countries have raised CBAM concerns in international forums, arguing it bypasses consensus-based climate governance.

3. Strategic Responses and Emerging Policy Pathways

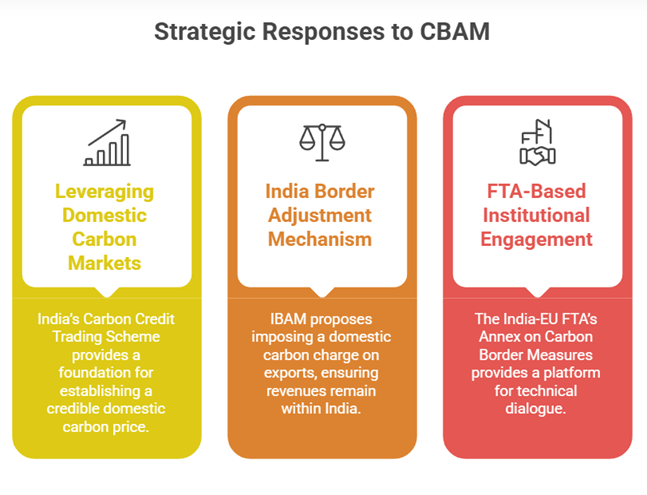

(a) Leveraging Domestic Carbon Markets

- India’s Carbon Credit Trading Scheme (CCTS) provides a foundation for establishing a credible domestic carbon price.

- Under CBAM Article 9, emissions already priced domestically can be deducted, creating scope to avoid double taxation.

- Example: If India ensures robust MRV (Monitoring, Reporting, Verification) standards, CCTS credits can be recognised at the EU border.

(b) India Border Adjustment Mechanism (IBAM) as Counter-Strategy

- IBAM proposes imposing a domestic carbon charge on exports, ensuring revenues remain within India while being credited under CBAM.

- This approach transforms CBAM from an external burden into a domestically managed fiscal instrument.

- Case Study: Similar mechanisms are being explored by countries like Canada and Japan to align domestic industries with global carbon pricing regimes.

(c) FTA-Based Institutional Engagement

- The India-EU FTA’s Annex on Carbon Border Measures provides a platform for technical dialogue and policy coordination.

- The inclusion of a most-favoured-nation clause ensures India benefits from any flexibility granted to other countries.

- Example: Structured engagement can help standardise methodologies for exchange rate conversion, emissions accounting, and offset recognition, reducing compliance uncertainty.

Conclusion:

- CBAM represents a significant evolution in linking trade with climate policy, but its current design raises legitimate concerns regarding equity, sovereignty, and fairness. While it seeks to address carbon leakage, it simultaneously risks imposing disproportionate adjustment costs on developing economies, potentially undermining the foundational principle of climate justice.

- A balanced approach requires recognising domestic carbon efforts like India’s CCTS, enabling mutual recognition frameworks, and ensuring that carbon revenues contribute to global—not just regional—decarbonisation goals.

- With global climate finance needs estimated at over $1 trillion annually for developing countries, mechanisms like IBAM and structured FTA engagement can help realign incentives. Ultimately, a cooperative, transparent, and equitable framework is essential to ensure that the transition to a low-carbon economy remains both effective and just.