Disaster Finance in India – Need for Geography-Based Risk Assessment

Disaster Finance in India refers to the allocation of financial resources for preparedness, mitigation, response, and recovery in disaster-prone regions. In India, this is largely guided by Finance Commission transfers to the State Disaster Response Funds (SDRFs). While recent allocations have increased significantly—crossing ₹2 lakh crore for the latest award period—concerns persist regarding the methodology of distribution.

India ranks among the most disaster-prone countries globally, with nearly 85% of its area exposed to one or more hazards (earthquakes, floods, cyclones, droughts). Climate projections indicate increasing frequency and intensity of extreme events, especially along coastal belts and floodplains. In this context, a shift from a population (headcount)-based allocation to a geography-based risk assessment becomes critical for ensuring equitable and effective disaster resilience.

1. Limitations of the Headcount-Based Approach in Disaster Finance

1.1 Misrepresentation of ‘Exposure’

- The use of total population as a proxy for exposure ignores the spatial distribution of risk, leading to flawed outcomes.

- As per the IPCC framework, exposure is defined as the presence of people in hazard-prone locations, not simply aggregate population.

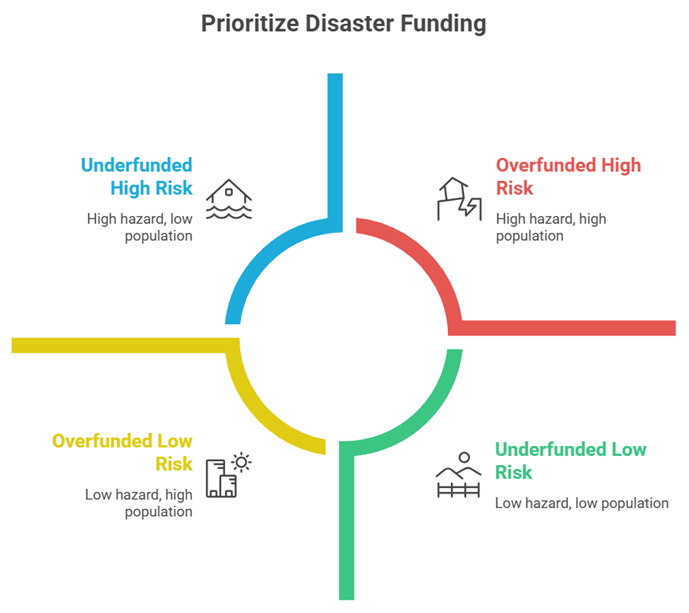

- Example: A densely populated inland State may receive higher funds despite being relatively safe, while a coastal State with fewer people but high cyclone exposure may be underfunded.

1.2 Distortion in Risk Index through Multiplicative Formula

- The shift to a multiplicative Disaster Risk Index (Hazard × Exposure × Vulnerability) theoretically aligns with disaster science, but operationalisation skews results.

- Large States like Uttar Pradesh and Bihar benefit disproportionately due to higher population scores, overshadowing high-hazard but smaller States.

- Case Study: Odisha, despite facing some of the most intense cyclones and investing in robust preparedness systems, sees a reduction in its relative share.

1.3 Inadequate Measurement of Vulnerability

- Vulnerability is proxied through per capita income (NSDP), which captures fiscal capacity but not structural vulnerability.

- This ignores intra-state disparities, quality of housing, healthcare access, and disaster preparedness.

- Example: Despite severe floods causing massive losses, Kerala is assigned low vulnerability due to higher income levels, masking real disaster risks.

2. Need for Geography-Based Risk Assessment in Disaster Finance

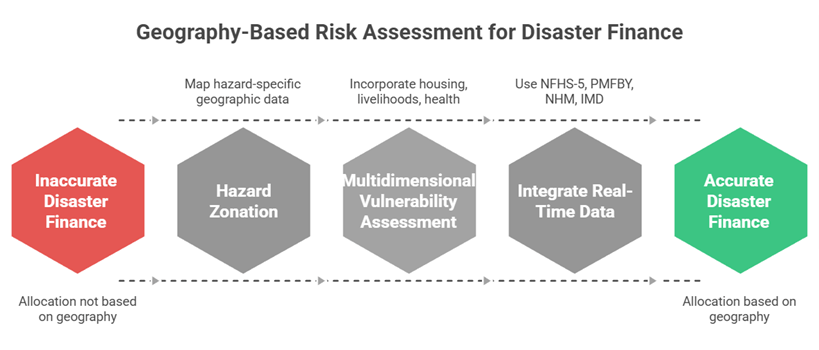

2.1 Scientific Measurement of Exposure through Hazard Zonation

- Exposure must be mapped using hazard-specific geographic data such as floodplains, seismic zones, and cyclone-prone coastal belts.

- Tools like the Vulnerability Atlas of India (BMTPC) and geospatial census mapping enable accurate estimation.

- Example: Coastal districts of Odisha and Andhra Pradesh face repeated cyclone landfalls, justifying higher allocation despite smaller populations.

2.2 Multidimensional Assessment of Vulnerability

- Vulnerability should incorporate indicators such as:

- Housing quality (kutcha vs pucca)

- Dependence on climate-sensitive livelihoods (agriculture, fisheries)

- Health infrastructure density in high-risk areas

- Case Study: Tribal regions in Jharkhand show high vulnerability due to poverty and remoteness, despite lower hazard frequency.

2.3 Integration of Real-Time Data and Institutional Mechanisms

- Data from NFHS-5, PMFBY coverage, NHM infrastructure, IMD early warning systems can provide dynamic inputs.

- Institutionalising a National Disaster Vulnerability Index, updated periodically, can standardise assessment.

- Example: Early warning dissemination systems in Odisha have drastically reduced cyclone mortality, reflecting improved adaptive capacity.

3. Policy Implications and Way Forward for Disaster Finance Reform

3.1 Aligning Financial Allocation with Climate Risk Realities

- Climate change is intensifying risks in coastal, drought-prone, and flood-prone regions, necessitating forward-looking finance models.

- States like Odisha, Assam, Kerala, and Andhra Pradesh are projected to face increasing disaster frequency.

- Example: The increasing frequency of extreme rainfall events in Kerala highlights the need for anticipatory funding.

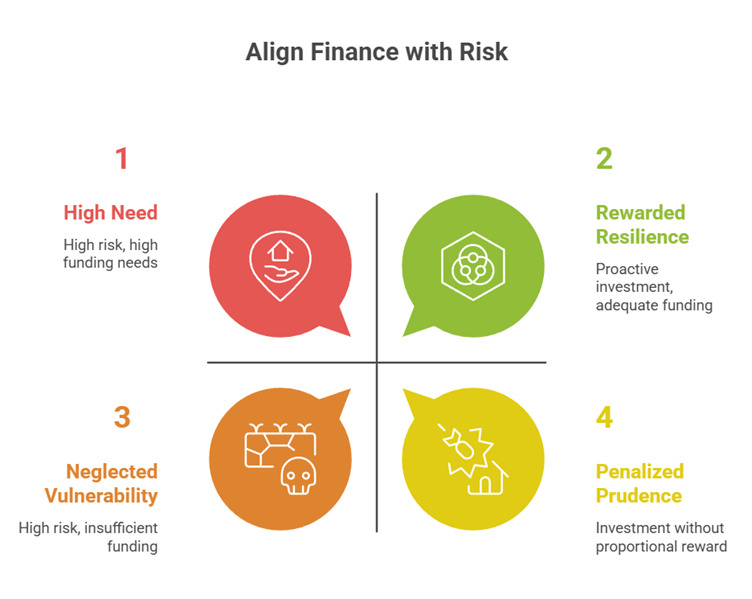

3.2 Incentivising Preparedness and Resilience Investments

- Current frameworks may penalise States that invest in disaster preparedness, as reduced vulnerability lowers their funding share.

- Finance mechanisms should reward:

- Effective early warning systems

- Evacuation infrastructure

- Community resilience programmes

- Case Study: Odisha’s near-zero cyclone mortality after investments in shelters and evacuation planning demonstrates successful risk reduction.

3.3 Strengthening Cooperative Federalism and Institutional Coordination

- Disaster management requires coordination between:

- National Disaster Management Authority (NDMA)

- State Disaster Management Authorities (SDMAs)

- A transparent, scientifically grounded allocation formula can reduce inter-state disparities and disputes.

- Example: Integration of centrally sponsored schemes like PMFBY and National Cyclone Risk Mitigation Project (NCRMP) with state-level planning enhances overall resilience.

Conclusion

India’s disaster finance architecture stands at a critical juncture as climate risks intensify across geographies. A headcount-based allocation model fails to capture the spatial realities of disaster risk, leading to inequitable and inefficient resource distribution. Transitioning to a geography-based, multidimensional risk assessment framework, grounded in hazard zonation, real exposure, and structural vulnerability, is essential.

With scientific tools, improved datasets, and institutional mechanisms already available, India can evolve towards a data-driven disaster finance system that not only responds to crises but anticipates them. Such a shift will ensure that financial resources are directed where they are most needed, strengthening resilience and safeguarding development gains in the decades ahead.

Recap: