Introduction

India’s economic vulnerability to external energy shocks is a growing concern in the context of global instability and rising crude oil prices.

Energy security refers to the uninterrupted availability of energy sources at an affordable price. India’s economic structure remains highly sensitive to external shocks due to its ~90% dependence on crude oil imports and significant reliance on fertilizer and natural gas imports.

Episodes such as the Russia-Ukraine conflict and disruptions in West Asia, including partial blockades in the Strait of Hormuz, have exposed structural vulnerabilities—reflected in rising current account deficit (CAD), inflationary pressures, and exchange rate volatility.

With the Indian crude basket breaching $120 per barrel in April 2026, far above a baseline of $70, macroeconomic stability faces tangible risks, underscoring the urgency of diversification and renewable transition.

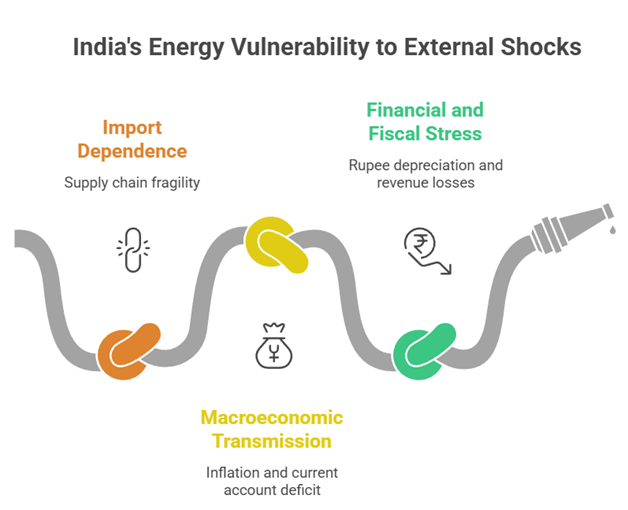

1. Nature and Extent of India’s Vulnerability to External Energy Shocks

(a) Import Dependence and Supply Chain Fragility

- Heavy reliance on imports from geopolitically sensitive regions makes India susceptible to supply disruptions and price volatility, especially when chokepoints like the Strait of Hormuz face instability.

- Despite diversification to 41 source countries, global price linkages mean domestic prices remain tied to Brent, WTI, and Dubai benchmarks, limiting insulation.

- Example: During the recent West Asian crisis, the Indian crude basket surged sharply, demonstrating how even diversified sourcing cannot prevent price shocks.

(b) Macroeconomic Transmission Channels

- Rising crude prices lead to cost-push inflation, increasing prices of petroleum products, fertilizers, and transport, with cascading effects on sectors like textiles, cement, and chemicals.

- The current account deficit widens as import bills rise while exports decline due to global slowdown; India’s exports to West Asia (~16% share) face demand compression.

- Example: RBI estimates suggest that a $50 increase above baseline crude prices can reduce GDP growth by ~1 percentage point and raise inflation by over 2 percentage points.

(c) Financial and Fiscal Stress

- Higher import bills increase demand for foreign exchange, causing rupee depreciation, aggravated by capital outflows (e.g., $13.6 billion FPI outflows in March 2026).

- Government faces pressure to maintain fuel subsidies and reduce excise duties, leading to significant revenue losses (~₹1.3 lakh crore annually under prolonged crisis conditions).

- Case Study: Oil Marketing Companies (OMCs) losses during price freezes highlight the fiscal burden of shielding consumers from global price spikes.

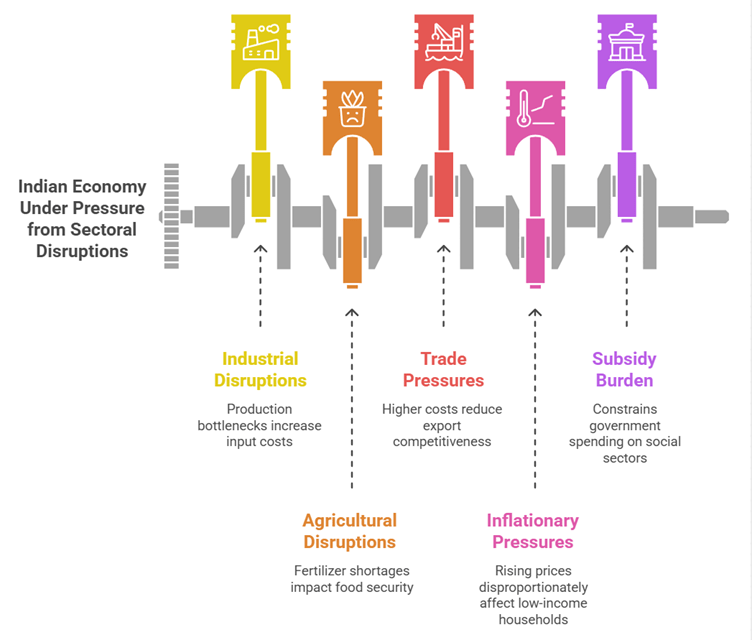

2. Sectoral and Structural Impacts on the Indian Economy

(a) Industrial and Agricultural Disruptions

- Energy-intensive industries experience production bottlenecks, affecting supply chains and increasing input costs.

- Fertilizer shortages directly impact agricultural productivity, particularly the Kharif season, threatening food security.

- Example: Rising global fertilizer prices post-conflict periods have historically led to reduced fertilizer usage by farmers, affecting yields.

(b) Trade and External Sector Pressures

- Export competitiveness is affected by higher logistics costs and reduced global demand, particularly in advanced economies like the U.S. and Europe.

- While rupee depreciation offers partial export advantage, it is offset by higher import costs and inflation.

- Case Study: During previous oil shocks (e.g., 2012–13), CAD surged beyond sustainable levels, triggering macroeconomic instability.

(c) Inflationary and Welfare Implications

- Rising energy prices translate into headline inflation, disproportionately affecting lower-income households due to higher expenditure on fuel and food.

- Increased subsidy burden constrains government spending on social sectors and capital expenditure.

- Example: Fuel price hikes have historically led to increased costs of public transport and essential commodities, amplifying inequality.

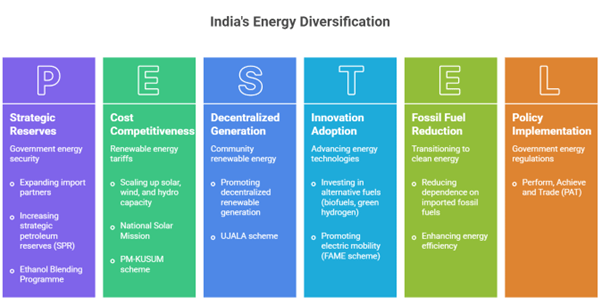

3. Need for Diversification and Renewable Energy Transition

(a) Energy Source Diversification

- Expanding import partners, increasing strategic petroleum reserves (SPR), and investing in alternative fuels (biofuels, green hydrogen) reduce vulnerability.

- Initiatives like Ethanol Blending Programme (target 20% blending) reduce crude dependence.

- Case Study: India’s SPR facilities in Visakhapatnam and Mangaluru helped buffer short-term supply disruptions.

(b) Accelerating Renewable Energy Adoption

- Scaling up solar, wind, and hydro capacity reduces dependence on imported fossil fuels; India targets 500 GW non-fossil capacity by 2030.

- Programs like National Solar Mission and PM-KUSUM scheme promote decentralized renewable generation in agriculture.

- Example: India has become one of the world’s largest solar energy producers, with solar tariffs becoming competitive with thermal power.

(c) Structural Reforms and Energy Efficiency

- Enhancing energy efficiency through schemes like Perform, Achieve and Trade (PAT) reduces overall consumption intensity.

- Promoting electric mobility (FAME scheme) reduces oil demand in the transport sector, which accounts for a major share of crude consumption.

- Case Study: LED adoption under the UJALA scheme significantly reduced electricity demand, demonstrating the impact of efficiency measures.

Conclusion

India’s exposure to global energy shocks is a structural reality, but not an irreversible one. With rising crude prices capable of shaving 1% off growth and pushing inflation upward significantly, the urgency for transition is evident.

A calibrated strategy combining diversification, renewable expansion, strategic reserves, and efficiency improvements can enhance resilience. As India moves toward its net-zero target by 2070 and expands non-fossil capacity, reducing external vulnerability will not only stabilize the economy but also align with long-term sustainable development goals.