“India’s clean energy rise is globally recognised, but its climate finance architecture remains fragile.” — Comment

Introduction

• India’s clean energy transition has emerged as one of the most significant global developments in recent years. With over 24.5 GW of solar capacity added in 2024, India is now the third-largest solar contributor globally after China and the US, and has been recognised by the UN Secretary-General’s Climate Report 2025 as a leading developing country in scaling renewable energy.

• The renewable sector already employs over a million people, contributing nearly 5% of GDP growth, and initiatives such as the International Solar Alliance (ISA) highlight India’s leadership in global energy governance. However, despite this progress, the climate finance architecture remains fragile, with an estimated requirement of $1.5–2.5 trillion by 2030, while current flows remain far below this benchmark. Commenting on this statement requires examining India’s achievements, the gaps in financing, and potential pathways to bridge this divide.

Body

• India’s Clean Energy Momentum

o Expansion of Renewable Energy Capacity

- India has crossed 190 GW of renewable capacity in 2024, with solar and wind being the largest contributors.

- Mega-projects such as Solar Park Scheme, KUSUM Yojana for decentralised solar pumps, and Green Hydrogen Mission show ambitious scaling.

- Example: Rewa Ultra Mega Solar Project (Madhya Pradesh) is a benchmark for low-cost solar tariffs.

o Global Leadership and Recognition

- India is a founding leader of the International Solar Alliance (ISA), with over 110 member countries.

- Its renewable expansion has been acknowledged in the IRENA 2024 outlook, projecting potential GDP growth of 2.8% annually till 2050 under a 1.5°C pathway.

- Example: India’s recognition at COP28 UAE for doubling non-fossil capacity well ahead of target.

o Employment and Inclusive Growth

- The renewable energy sector employed over 1 million people in 2023, with 80,000 employed in off-grid solar solutions alone.

- Decentralised solar grids in Bihar and Uttar Pradesh showcase how renewable expansion enables rural electrification and jobs.

- Government initiatives like Skill Council for Green Jobs are preparing manpower for solar, wind and green hydrogen industries.

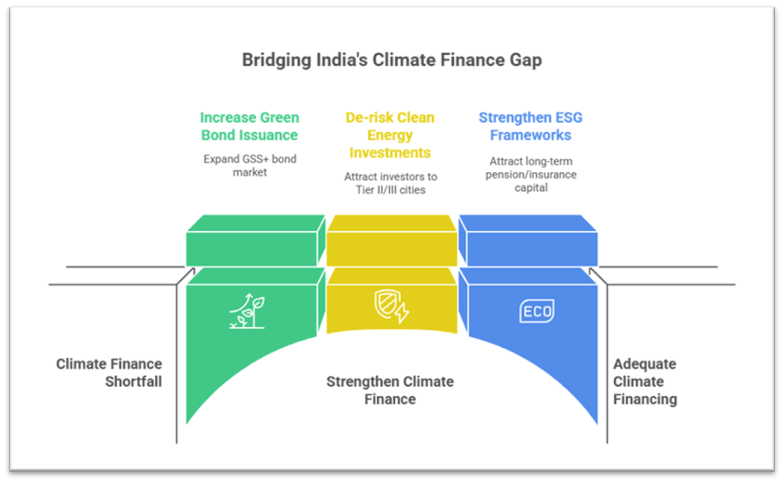

• The Fragility of Climate Finance Architecture

o Climate Finance Gap

- India requires between $1.5–2.5 trillion by 2030 for a 1.5°C-aligned growth trajectory, but current financing remains limited.

- By 2024, GSS+ (Green, Social, Sustainability, and Sustainability-linked) bond issuance stood at $55.9 billion, but this is only a fraction of what is required.

- Example: Despite success in sovereign green bonds (₹16,000 crore issued in 2023), inflows are skewed towards large corporates, excluding MSMEs.

o Private Sector Dominance and Limitations

- Nearly 84% of green bond issuance came from private corporates, leaving limited access for smaller firms.

- High risks deter investors from clean energy in Tier II and III cities and rural infrastructure.

- Example: Many agrivoltaics projects and local EV charging networks face credit constraints despite proven feasibility.

o Institutional and Regulatory Constraints

- Indian institutional investors like EPFO and LIC still lack clear regulatory guidelines to invest in climate-aligned projects.

- Weak environmental, social and governance (ESG) frameworks restrict long-term pension or insurance capital from entering.

- Example: In contrast, Norway’s Sovereign Wealth Fund allocates over 10% to ESG-linked assets, while India lags behind.

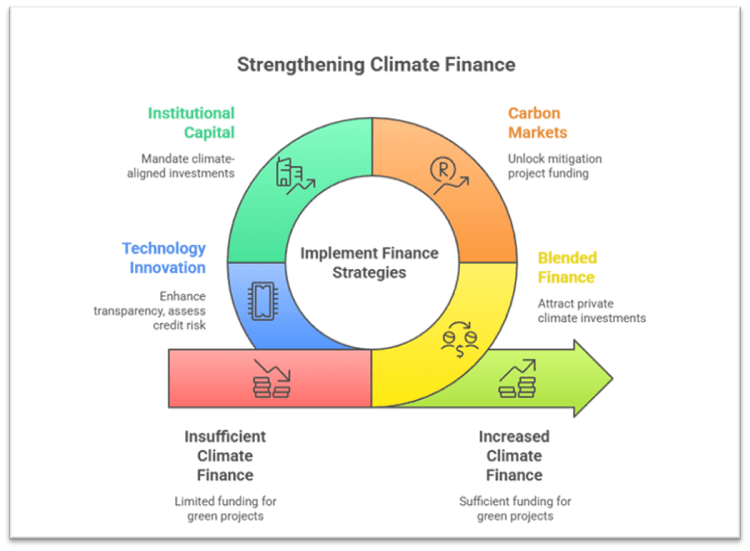

• Strategies to Strengthen Climate Finance

o Blended and Risk-Sharing Finance

- Credit enhancement tools like partial guarantees, subordinated debt and performance-linked guarantees can attract private finance.

- Example: World Bank–backed partial risk guarantees helped solar parks in Rajasthan reduce investor concerns.

- State governments can use fiscal incentives and targeted subsidies to attract mid-sized players.

o Tapping Carbon Markets

- India launched its Carbon Credit Trading Scheme (2023), which if transparent, could unlock billions for mitigation projects.

- Pilot projects in Maharashtra’s sugar industry show potential of carbon trading in decarbonising traditional sectors.

- Example: European ETS model offers lessons in pricing carbon effectively.

o Unlocking Domestic Institutional Capital

- Pension funds and insurers can be mandated to invest a proportion (say 5–10%) in climate-aligned projects.

- Regulatory clarity on ESG guidelines and long-term project pipelines can build investor confidence.

- Example: National Infrastructure Investment Fund (NIIF) could be scaled for green financing pools.

o Technology and Innovation in Finance

- Blockchain can be used for tracking climate finance flows to ensure transparency.

- Artificial Intelligence-driven models can assess credit risk of green projects more accurately.

- Example: Singapore’s Green Finance Centre already uses AI-based green risk modelling, which India can replicate.

Conclusion

• India’s clean energy rise is globally acknowledged, with rapid solar expansion, global partnerships, and visible economic and employment gains. Yet, without robust climate finance architecture, the momentum risks slowing. Bridging the gap requires trillions in capital mobilisation, innovative blended finance, regulatory reforms to unlock institutional investors, and effective use of carbon markets and technology-driven finance mechanisms.

• If achieved, India could not only meet its 2030 targets of 500 GW non-fossil capacity but also emerge as the world’s foremost clean energy hub. The way forward lies in aligning finance with ambition, ensuring that India’s transition remains inclusive, sustainable, and globally competitive.

Recap: