India’s Low Corporate R&D: Market Failure or Risk Aversion? A Critical Analysis

India’s low corporate R&D intensity remains a major concern despite the country being one of the fastest-growing major economies. Understanding whether India’s low corporate R&D is primarily driven by market failure rather than mere risk aversion is crucial for improving innovation productivity and technological competitiveness in the Indian private sector.

Introduction

- Research and Development (R&D) refers to systematic creative work undertaken to increase the stock of knowledge and devise new applications. It is widely regarded as a core driver of productivity growth, technological upgrading, and long-term competitiveness.

- Despite being one of the fastest-growing major economies, India’s Gross Expenditure on R&D (GERD) remains around 0.6–0.7% of GDP, with corporate R&D intensity stagnating near 0.23% of GDP, far below economies such as South Korea (above 4%), China (above 2.5%), and the OECD average (around 2.7%).

- Surveys on innovation ecosystems and global competitiveness consistently show that while India performs well in start-up dynamism and digital public infrastructure, it lags in private-sector R&D depth and high-technology commercialization.

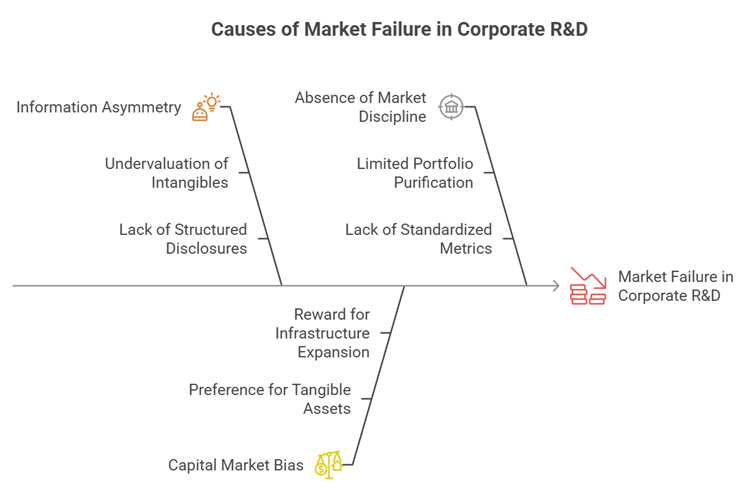

I. Market Failure and Information Asymmetry in Corporate R&D

1. Information Asymmetry and Undervaluation of Intangibles

- When investors cannot distinguish between high-quality and low-quality innovation projects, they discount all firms similarly, leading to systematic undervaluation of genuine R&D-intensive firms.

- In the absence of structured disclosures on patent pipelines, technology readiness levels, or innovation turnover, capital markets struggle to price intangible assets effectively.

- Example – Pharmaceutical Sector in India: Several mid-sized pharma firms with strong research pipelines face volatile valuations because pipeline maturity and clinical-stage data are not transparently standardized, discouraging long-gestation research investments.

2. Capital Market Bias Toward Tangible Assets

- Evidence across countries shows that improved innovation disclosures tend to increase R&D intensity without proportionately increasing capital expenditure on physical assets, suggesting that transparency redirects capital toward risky but productive innovation.

- Indian capital markets often reward firms with visible infrastructure expansion more readily than those investing in long-term technological bets.

- Case Study – IT Services vs Deep-Tech Firms: Traditional IT service firms with predictable revenue models have historically attracted more stable investment compared to deep-tech hardware or semiconductor design firms that require patient capital and longer gestation.

3. Absence of Market Discipline and Quality Filtering

- Structured disclosure acts as a mechanism for portfolio purification, enabling investors and competitors to evaluate project quality and prune duplicative or low-value innovation.

- Without standardized metrics, there is limited external discipline to eliminate rent-seeking or imitation-based innovation projects.

- Example – Global Experience in East Asia: Countries that introduced mandatory intangible reporting frameworks observed not only higher R&D spending but improved efficiency, as weaker projects were rationally discontinued early.

II. Structural Constraints Beyond Pure Risk Aversion

1. High Uncertainty and Long Gestation Periods

- Innovation is inherently uncertain, especially in biotechnology, clean energy, advanced materials, and semiconductors.

- In developing financial ecosystems, long-gestation projects face liquidity and refinancing risks.

- Example – Semiconductor Manufacturing Initiatives: Despite government incentives under the Production-Linked Incentive (PLI) scheme, private investment hesitancy reflects high capital intensity and uncertain global competition, compounded by valuation uncertainty.

2. Weak Linkages Between Industry and Academia

- A large share of India’s R&D expenditure comes from the public sector, unlike advanced economies where private firms dominate.

- Limited industry–university collaboration constrains knowledge transfer and commercialization.

- Case Study – Biotechnology Clusters: Successful clusters like Bengaluru’s biotech ecosystem show that where academic linkages, venture capital, and incubators align, innovation intensity improves significantly.

3. Financial Constraints and Cost of Capital

- Firms dependent on equity markets face higher costs of capital when intangible assets are poorly understood.

- Small and medium enterprises engaged in innovation face limited access to long-term credit due to absence of collateralizable assets.

III. Measures to Improve Innovation Productivity in the Private Sector

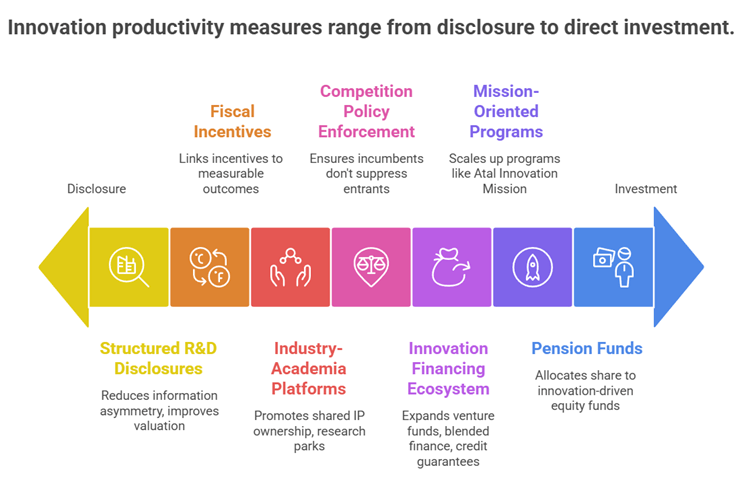

1. Mandatory Structured R&D and Technology Disclosures

- Introduce standardized reporting under securities regulations covering:

- R&D expenditure with segment-level granularity

- Patent filings, grants, expirations

- Technology workforce composition

- Technology Readiness Levels (TRL)

- Innovation turnover (revenue from products introduced in the last five years)

- A phased voluntary-to-mandatory transition would build data quality without abrupt compliance shocks.

- Expected Impact: Reduction in information asymmetry, improved valuation of innovation-intensive firms, and enhanced shareholder discipline.

2. Strengthening Innovation Financing Ecosystem

- Expand deep-tech focused venture funds, blended finance models, and innovation-linked credit guarantees.

- Scale up mission-oriented programs such as:

- Atal Innovation Mission

- National Research Foundation (NRF)

- PLI schemes targeting sunrise sectors

- Encourage pension and insurance funds to allocate a small share toward innovation-driven equity funds to provide patient capital.

- Example – Digital Public Infrastructure (DPI): The success of UPI and Aadhaar-enabled ecosystems demonstrates how public investment in foundational innovation can crowd in private technological development.

3. Improving Innovation Productivity and Efficiency

- Link fiscal incentives (such as weighted tax deductions for R&D) to measurable outcomes like patent quality, commercialization rates, or export performance.

- Promote industry–academia collaborative platforms through shared IP ownership models and research parks.

- Enhance competition policy enforcement to ensure incumbents do not suppress disruptive entrants.

Conclusion

- India’s low corporate R&D intensity cannot be reduced to mere risk aversion; it reflects a deeper market failure rooted in information asymmetry, mispricing of intangible assets, weak disclosure norms, and financing constraints. When innovation remains invisible, it is undervalued; when undervalued, it is underproduced.

- A calibrated reform strategy—anchored in structured disclosure standards, innovation-sensitive capital markets, stronger industry–academia linkages, and patient risk capital mechanisms—can transform the innovation landscape. With India aspiring to become a $5 trillion economy and a global manufacturing and technology hub, raising corporate R&D intensity even to 1% of GDP would significantly enhance productivity growth and export sophistication.

- By ensuring that markets can clearly see and evaluate innovation quality, India can shift from incremental imitation to high-value, research-led industrial transformation, fostering sustainable growth, technological sovereignty, and improved social outcomes.

Recap: