Contribution to GSDP Criterion in 16th Finance Commission: Impact on Horizontal Devolution and Fiscal Federalism

Contribution to GSDP Criterion in 16th Finance Commission represents a significant shift in India’s fiscal federal framework. The introduction of this parameter into the horizontal devolution formula reflects evolving debates between equity and efficiency in intergovernmental fiscal transfers.

Introduction

- The Finance Commission (FC) is a constitutional body established under Article 280 to recommend the distribution of tax revenues between the Union and the States (vertical devolution) and among States themselves (horizontal devolution) to ensure fiscal federalism and balanced regional development.

- Horizontal devolution traditionally prioritizes equity-based criteria such as income distance, population, area, forest cover, and fiscal discipline, reflecting the principle of equalization—that all States should be able to provide comparable levels of public services. With States collectively accounting for nearly 62% of government expenditure but raising only about 38–40% of total revenues, intergovernmental transfers remain essential for fiscal stability and national cohesion.

- The introduction of ‘Contribution to Gross State Domestic Product (GSDP)’ as a criterion by the Sixteenth Finance Commission marks a shift toward incorporating efficiency and performance considerations into resource distribution, reflecting evolving debates between equity and efficiency in fiscal federalism.

Body

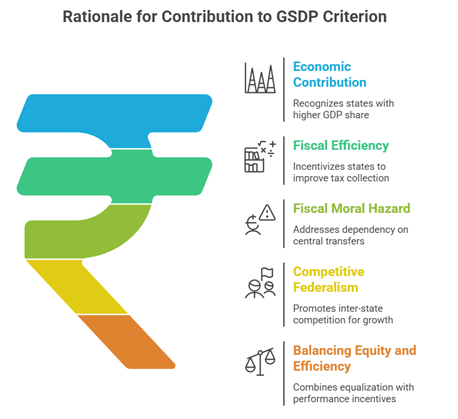

I. Rationale Behind Introducing ‘Contribution to GSDP’ Criterion

1. Reflecting Economic Contribution and Fiscal Efficiency

- The inclusion of Contribution to GSDP seeks to recognize States that contribute more to the national economy, aligning fiscal transfers with economic productivity and efficiency, thereby incentivizing States to enhance their growth potential.

- Since economically advanced States such as Maharashtra, Tamil Nadu, and Karnataka contribute significantly to national tax revenues through GST collections, corporate taxes, and consumption, this criterion acknowledges their role in sustaining national fiscal capacity.

- Example: Case Study – Maharashtra contributes around 14–15% of India’s GDP, yet its share in tax devolution has historically been lower relative to its contribution, leading to persistent demands for recognizing economic performance.

2. Addressing Concerns of ‘Fiscal Moral Hazard’

- Traditional criteria such as income distance favor poorer States, which ensures equity but may weaken incentives for States to improve their tax base and economic efficiency, potentially creating dependency on central transfers.

- By introducing a performance-linked parameter, the Commission attempts to promote competitive federalism, encouraging States to improve governance, infrastructure, and economic productivity.

- Example: Real-life Example – Tamil Nadu’s investments in manufacturing clusters like Sriperumbudur and Karnataka’s IT ecosystem in Bengaluru demonstrate how growth-oriented policies enhance economic contribution.

3. Balancing Equity with Efficiency in Fiscal Federalism

- The new criterion reflects a shift toward combining equalization objectives with performance incentives, ensuring that transfers do not solely compensate backwardness but also reward economic efficiency.

- It aligns with broader reforms such as the GST regime, which aims to create a unified national market and encourage States to expand their tax bases.

- Example: Government Initiative – The ‘Ease of Doing Business’ reforms and PM Gati Shakti infrastructure program aim to enhance productivity across States, making economic contribution a relevant indicator for fiscal allocation.

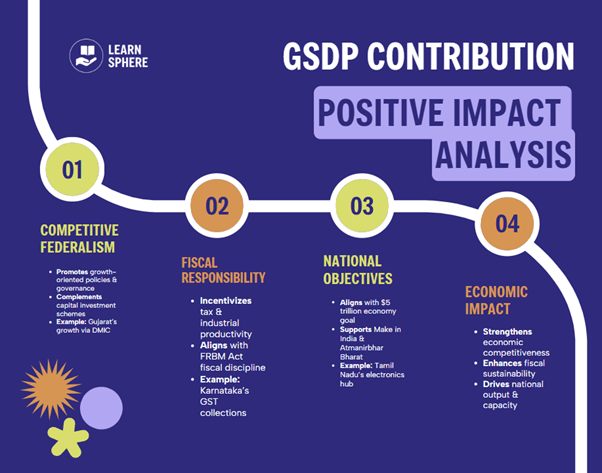

II. Potential Positive Impact of Contribution to GSDP Criterion

1. Promoting Competitive and Cooperative Federalism

- Recognizing economic contribution encourages States to adopt growth-oriented policies, improve governance, and enhance investment attractiveness, strengthening India’s overall economic competitiveness.

- It complements performance-based schemes like the Scheme for Special Assistance to States for Capital Investment, which incentivizes infrastructure spending.

- Example: Case Study – Gujarat’s industrial growth through the Delhi-Mumbai Industrial Corridor (DMIC) increased its share in national manufacturing output, demonstrating how productivity-linked incentives drive growth.

2. Encouraging Efficient Use of Resources and Fiscal Responsibility

- The criterion incentivizes States to improve tax administration, industrial productivity, and fiscal management, reducing reliance on transfers and enhancing fiscal sustainability.

- It aligns with fiscal discipline frameworks such as the Fiscal Responsibility and Budget Management (FRBM) Act, encouraging prudent financial management.

- Example: Real-life Example – Karnataka’s strong GST collections driven by its technology sector reflect efficient economic and fiscal systems contributing to national revenues.

3. Aligning Transfers with National Economic Objectives

- By recognizing economic contribution, transfers become more consistent with India’s goal of becoming a $5 trillion economy, where economically productive regions play a key role.

- It supports national initiatives such as Make in India and Atmanirbhar Bharat, which depend on State-level economic performance.

- Example: Case Study – Tamil Nadu’s electronics manufacturing hub, supported by Production Linked Incentive (PLI) schemes, enhances both national output and fiscal capacity.

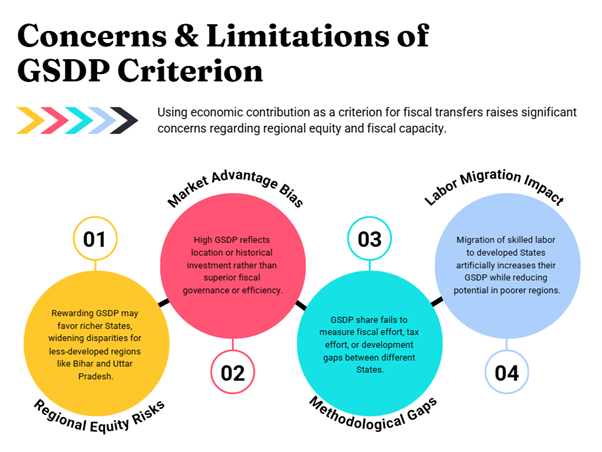

III. Concerns and Limitations of Using Contribution to GSDP Criterion

1. Risk of Undermining Equalization and Regional Equity

- Fiscal transfers are meant to address structural inequalities, but rewarding economic contribution may disproportionately favor richer States, widening disparities between developed and less-developed regions.

- Less developed States such as Bihar and Uttar Pradesh, with lower industrial bases, may receive reduced allocations despite having greater developmental needs.

- Example: Case Study – Bihar has a per capita income less than one-third of the national average, yet it requires substantial fiscal support to improve education, health, and infrastructure.

2. Economic Contribution Does Not Fully Reflect Fiscal Capacity

- High GSDP contribution may reflect market advantages, geographic location, or historical investments, rather than superior fiscal governance or policy efficiency.

- Migration of skilled labor and capital to developed States artificially increases their economic contribution while reducing the growth potential of poorer States.

- Example: Real-life Example – Skilled workers migrating from eastern States to southern and western States contribute to economic growth there but do not necessarily reflect the originating State’s fiscal inefficiency.

3. Methodological and Conceptual Limitations

- Using GSDP share as a proxy for efficiency may not accurately measure fiscal effort or governance quality, as it does not consider tax effort, social needs, or development gaps.

- The discontinuation of criteria such as fiscal discipline and revenue deficit grants reduces the ability to address State-specific needs and equalization objectives.

- Example: Government Framework – Article 275 provides for need-based grants to States, recognizing that fiscal transfers must address disparities in service delivery rather than purely economic output.

Conclusion

- The introduction of ‘Contribution to GSDP’ as a criterion represents an important evolution in India’s fiscal federal framework, reflecting the need to balance equity with efficiency and performance incentives. While it promotes competitive federalism, economic efficiency, and fiscal responsibility, its impact must be carefully calibrated to avoid undermining the constitutional objective of equalization and balanced regional development.

- With regional disparities still significant—as reflected in per capita income differences of over three times between richer and poorer States—fiscal transfers must continue to prioritize inclusive growth alongside performance incentives.

- A balanced approach combining income distance, fiscal discipline, and performance indicators, along with strengthened equalization grants and transparent methodology, can ensure that fiscal federalism remains both equitable and growth-oriented, supporting India’s long-term development and national unity.

I. Rationale Behind Introducing ‘Contribution to GSDP’ Criterion

1. Reflecting Economic Contribution and Fiscal Efficiency

- The inclusion of Contribution to GSDP seeks to recognize States that contribute more to the national economy, aligning fiscal transfers with economic productivity and efficiency, thereby incentivizing States to enhance their growth potential.

- Since economically advanced States such as Maharashtra, Tamil Nadu, and Karnataka contribute significantly to national tax revenues through GST collections, corporate taxes, and consumption, this criterion acknowledges their role in sustaining national fiscal capacity.

- Example: Case Study – Maharashtra contributes around 14–15% of India’s GDP, yet its share in tax devolution has historically been lower relative to its contribution, leading to persistent demands for recognizing economic performance.

2. Addressing Concerns of ‘Fiscal Moral Hazard’

- Traditional criteria such as income distance favor poorer States, which ensures equity but may weaken incentives for States to improve their tax base and economic efficiency, potentially creating dependency on central transfers.

- By introducing a performance-linked parameter, the Commission attempts to promote competitive federalism, encouraging States to improve governance, infrastructure, and economic productivity.

- Example: Real-life Example – Tamil Nadu’s investments in manufacturing clusters like Sriperumbudur and Karnataka’s IT ecosystem in Bengaluru demonstrate how growth-oriented policies enhance economic contribution.

3. Balancing Equity with Efficiency in Fiscal Federalism

- The new criterion reflects a shift toward combining equalization objectives with performance incentives, ensuring that transfers do not solely compensate backwardness but also reward economic efficiency.

- It aligns with broader reforms such as the GST regime, which aims to create a unified national market and encourage States to expand their tax bases.

- Example: Government Initiative – The ‘Ease of Doing Business’ reforms and PM Gati Shakti infrastructure program aim to enhance productivity across States, making economic contribution a relevant indicator for fiscal allocation.

II. Potential Positive Impact of Contribution to GSDP Criterion

1. Promoting Competitive and Cooperative Federalism

- Recognizing economic contribution encourages States to adopt growth-oriented policies, improve governance, and enhance investment attractiveness, strengthening India’s overall economic competitiveness.

- It complements performance-based schemes like the Scheme for Special Assistance to States for Capital Investment, which incentivizes infrastructure spending.

- Example: Case Study – Gujarat’s industrial growth through the Delhi-Mumbai Industrial Corridor (DMIC) increased its share in national manufacturing output, demonstrating how productivity-linked incentives drive growth.

2. Encouraging Efficient Use of Resources and Fiscal Responsibility

- The criterion incentivizes States to improve tax administration, industrial productivity, and fiscal management, reducing reliance on transfers and enhancing fiscal sustainability.

- It aligns with fiscal discipline frameworks such as the Fiscal Responsibility and Budget Management (FRBM) Act, encouraging prudent financial management.

- Example: Real-life Example – Karnataka’s strong GST collections driven by its technology sector reflect efficient economic and fiscal systems contributing to national revenues.

3. Aligning Transfers with National Economic Objectives

- By recognizing economic contribution, transfers become more consistent with India’s goal of becoming a $5 trillion economy, where economically productive regions play a key role.

- It supports national initiatives such as Make in India and Atmanirbhar Bharat, which depend on State-level economic performance.

- Example: Case Study – Tamil Nadu’s electronics manufacturing hub, supported by Production Linked Incentive (PLI) schemes, enhances both national output and fiscal capacity.

III. Concerns and Limitations of Using Contribution to GSDP Criterion

1. Risk of Undermining Equalization and Regional Equity

- Fiscal transfers are meant to address structural inequalities, but rewarding economic contribution may disproportionately favor richer States, widening disparities between developed and less-developed regions.

- Less developed States such as Bihar and Uttar Pradesh, with lower industrial bases, may receive reduced allocations despite having greater developmental needs.

- Example: Case Study – Bihar has a per capita income less than one-third of the national average, yet it requires substantial fiscal support to improve education, health, and infrastructure.

2. Economic Contribution Does Not Fully Reflect Fiscal Capacity

- High GSDP contribution may reflect market advantages, geographic location, or historical investments, rather than superior fiscal governance or policy efficiency.

- Migration of skilled labor and capital to developed States artificially increases their economic contribution while reducing the growth potential of poorer States.

- Example: Real-life Example – Skilled workers migrating from eastern States to southern and western States contribute to economic growth there but do not necessarily reflect the originating State’s fiscal inefficiency.

3. Methodological and Conceptual Limitations

- Using GSDP share as a proxy for efficiency may not accurately measure fiscal effort or governance quality, as it does not consider tax effort, social needs, or development gaps.

- The discontinuation of criteria such as fiscal discipline and revenue deficit grants reduces the ability to address State-specific needs and equalization objectives.

- Example: Government Framework – Article 275 provides for need-based grants to States, recognizing that fiscal transfers must address disparities in service delivery rather than purely economic output.

Conclusion

- The introduction of ‘Contribution to GSDP’ as a criterion represents an important evolution in India’s fiscal federal framework, reflecting the need to balance equity with efficiency and performance incentives. While it promotes competitive federalism, economic efficiency, and fiscal responsibility, its impact must be carefully calibrated to avoid undermining the constitutional objective of equalization and balanced regional development.

- With regional disparities still significant—as reflected in per capita income differences of over three times between richer and poorer States—fiscal transfers must continue to prioritize inclusive growth alongside performance incentives.

- A balanced approach combining income distance, fiscal discipline, and performance indicators, along with strengthened equalization grants and transparent methodology, can ensure that fiscal federalism remains both equitable and growth-oriented, supporting India’s long-term development and national unity.

Recap: