Introduction:

- Climate finance refers to local, national and transnational financing—drawn from public, private and alternative sources—that supports mitigation and adaptation actions addressing climate change.

- India’s updated Nationally Determined Contributions (NDCs) aim to reduce the emissions intensity of GDP by 45% from 2005 levels by 2030, achieve about 50% cumulative electric power installed capacity from non-fossil fuel sources, and create an additional carbon sink of 2.5–3 billion tonnes of CO₂ equivalent through forest and tree cover.

- Achieving these goals requires massive investments, with estimates suggesting India needs over ₹162 lakh crore by 2030 and more than $10 trillion by 2070 for its net-zero pathway. The central challenge increasingly lies not in the absence of capital globally, but in building institutions capable of mobilizing, directing and scaling finance efficiently.

Body:

I. Why institutional architecture has emerged as the principal constraint

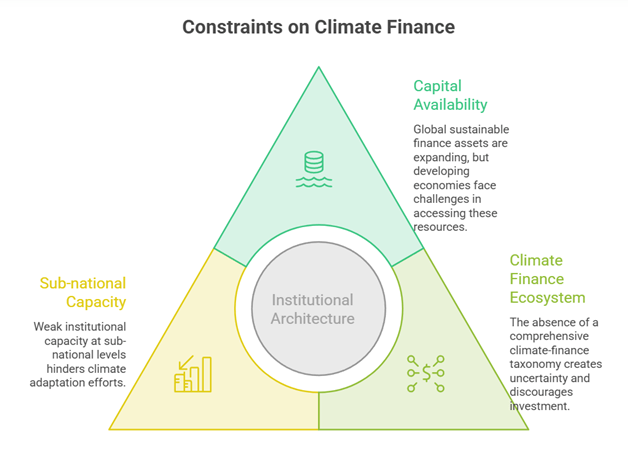

A. Availability of capital but limitations in financial intermediation

- Global sustainable finance assets and climate-focused investment funds have expanded significantly, yet developing economies continue to face difficulties in accessing these resources due to fragmented financial channels and project-preparation bottlenecks.

- India has witnessed rapid growth in green bonds, sovereign green bonds, sustainability-linked bonds and ESG investments, demonstrating that investor appetite exists; however, bankable projects remain limited due to weak institutional pipelines.

- Example – Sovereign Green Bond Programme: Government issuances have successfully attracted investors and established pricing benchmarks, but overall climate finance mobilization remains far below sectoral requirements.

B. Absence of a comprehensive climate-finance ecosystem

- Lack of a fully operational Climate Finance Taxonomy creates uncertainty regarding what qualifies as a green activity, discouraging institutional investors and increasing risks of greenwashing.

- Inadequate mechanisms for project verification, monitoring and disclosure increase transaction costs and reduce investor confidence.

- Case Study – European Union Taxonomy: Standardized classification systems have significantly improved capital flows into sustainable sectors by reducing information asymmetry and enhancing regulatory certainty.

C. Weak institutional capacity at sub-national levels

- Climate adaptation requirements are highly localized, yet States and urban local bodies often lack expertise to structure climate projects, issue green debt instruments or access international climate funds.

- Fiscal constraints and limited technical capacity prevent climate-sensitive regions from leveraging available financial opportunities.

- Example – Coastal resilience initiatives in Odisha and ecosystem restoration programmes in Himalayan States: Ambitious adaptation projects frequently depend on external support because institutional mechanisms for climate finance access remain underdeveloped.

II. Institutional reforms already strengthening India’s climate-finance architecture

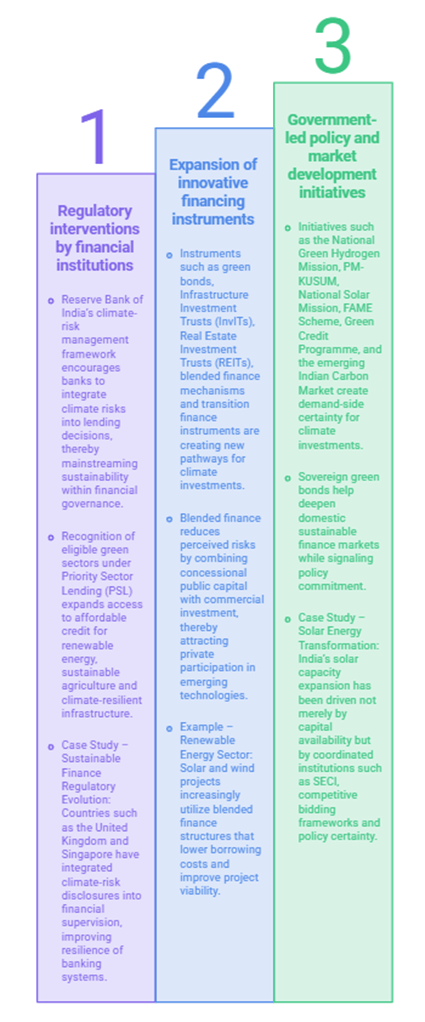

A. Regulatory interventions by financial institutions

- The Reserve Bank of India’s climate-risk management framework encourages banks to integrate climate risks into lending decisions, thereby mainstreaming sustainability within financial governance.

- Recognition of eligible green sectors under Priority Sector Lending (PSL) expands access to affordable credit for renewable energy, sustainable agriculture and climate-resilient infrastructure.

- Case Study – Sustainable Finance Regulatory Evolution: Countries such as the United Kingdom and Singapore have integrated climate-risk disclosures into financial supervision, improving resilience of banking systems.

B. Expansion of innovative financing instruments

- Instruments such as green bonds, Infrastructure Investment Trusts (InvITs), Real Estate Investment Trusts (REITs), blended finance mechanisms and transition finance instruments are creating new pathways for climate investments.

- Blended finance reduces perceived risks by combining concessional public capital with commercial investment, thereby attracting private participation in emerging technologies.

- Example – Renewable Energy Sector: Solar and wind projects increasingly utilize blended finance structures that lower borrowing costs and improve project viability.

C. Government-led policy and market development initiatives

- Initiatives such as the National Green Hydrogen Mission, PM-KUSUM, National Solar Mission, FAME Scheme, Green Credit Programme, and the emerging Indian Carbon Market create demand-side certainty for climate investments.

- Sovereign green bonds help deepen domestic sustainable finance markets while signaling policy commitment.

- Case Study – Solar Energy Transformation: India’s solar capacity expansion has been driven not merely by capital availability but by coordinated institutions such as SECI, competitive bidding frameworks and policy certainty.

III. Institutional measures required to achieve the 2030 NDC targets

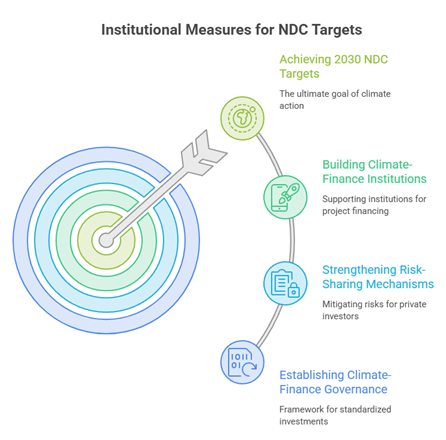

A. Establishing a robust climate-finance governance framework

- Immediate operationalization of a nationally accepted Climate Finance Taxonomy is essential for standardizing investments, preventing greenwashing and improving investor confidence.

- Mandatory climate disclosures aligned with global sustainability standards can improve transparency and capital allocation efficiency.

- Example – International Sustainability Reporting Standards: Standardized disclosure frameworks have enhanced comparability and accountability across jurisdictions.

B. Strengthening risk-sharing and credit-enhancement mechanisms

- Climate projects often face technology, regulatory and market risks that deter private investors despite long-term viability.

- Public guarantees, first-loss facilities, viability-gap funding and blended finance platforms can significantly crowd in private capital.

- Case Study – Green Hydrogen Projects: Early-stage investments require risk-mitigation mechanisms because high upfront costs and uncertain market demand limit commercial financing.

C. Building federal and local climate-finance institutions

- Establishment of a dedicated State Climate Finance Facility could support States and municipalities in project preparation, capacity building and access to green debt markets.

- Strengthening institutions such as NABARD, SIDBI, and State-level climate cells can improve financing for adaptation and resilience projects.

- Example – Climate-Resilient Agriculture: Localized investments in drought-proofing, watershed management and resilient cropping systems require decentralized institutions capable of aggregating projects and mobilizing finance.

Conclusion:

- India’s climate challenge is fundamentally becoming an institutional mobilization challenge rather than a pure resource challenge. The country has demonstrated the ability to attract green investments, expand renewable energy and develop innovative financial instruments.

- However, achieving the 2030 NDC targets will require a robust climate-finance taxonomy, stronger regulatory incentives, deeper risk-sharing mechanisms and empowered State-level institutions.

- With climate-related investments needing an estimated additional 2.5% of GDP annually until 2030, the decisive factor will be how effectively institutions convert available capital into scalable mitigation and adaptation outcomes. A coherent institutional architecture can transform India from a climate-finance recipient into a global model for financing sustainable development in emerging economies.