Introduction:

- Financial inclusion refers to ensuring access to affordable and timely financial services—banking, credit, insurance, and pensions—to vulnerable sections, especially women and rural populations. Over the past decade, India has witnessed a structural expansion of financial inclusion through initiatives like Pradhan Mantri Jan Dhan Yojana (PMJDY), which has opened over 57 crore bank accounts, with women holding a majority share, thereby integrating them into the formal financial ecosystem.

- Simultaneously, the Self-Help Group (SHG) movement, institutionalized under the Deendayal Antyodaya Yojana–National Rural Livelihoods Mission (DAY-NRLM), has mobilized nearly 10 crore women into over 90 lakh groups, transforming them into agents of local economic activity. This convergence has created a “multiplier effect”, wherein financial access translates into entrepreneurship, income generation, and broader socio-economic transformation.

Body:

· 1. Financial Inclusion as a Catalyst for Grassroots Economic Expansion

o 1.1 Expansion of Formal Financial Access and Savings Culture

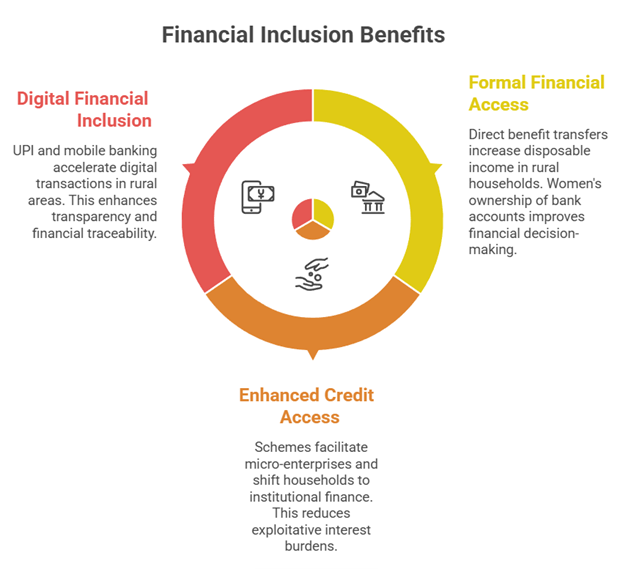

- The PMJDY–Aadhaar–Mobile (JAM) trinity has enabled direct benefit transfers, reducing leakages and ensuring last-mile delivery of welfare, thereby increasing disposable income in rural households.

- Women’s ownership of bank accounts has improved intra-household financial decision-making, contributing to better outcomes in health, nutrition, and education.

- Example: In states like Jharkhand and Odisha, DBT-linked accounts have enhanced timely access to schemes like PM-KISAN and MGNREGA wages, stabilizing rural consumption patterns.

o 1.2 Enhanced Credit Access and Entrepreneurial Ecosystem

- Schemes like Pradhan Mantri MUDRA Yojana (PMMY), with nearly 70% of loans going to women, have facilitated micro-enterprises in sectors such as tailoring, food processing, and retail.

- Increased credit penetration has shifted households from informal moneylenders to institutional finance, reducing exploitative interest burdens.

- Case Study: Women entrepreneurs in Tamil Nadu’s dairy cooperatives leveraged MUDRA loans to scale operations, contributing to local supply chains and employment.

o 1.3 Digital Financial Inclusion and Economic Formalization

- The rise of Unified Payments Interface (UPI) and mobile banking has accelerated digital transactions even in rural areas, enhancing transparency and financial traceability.

- Digital inclusion has enabled small vendors and SHG members to participate in e-commerce and digital marketplaces, linking rural economies to national supply chains.

- Example: SHG products marketed via GeM (Government e-Marketplace) and platforms like Amazon Saheli have expanded market access.

2. SHG Movement as a Driver of Collective Empowerment and Local Economies

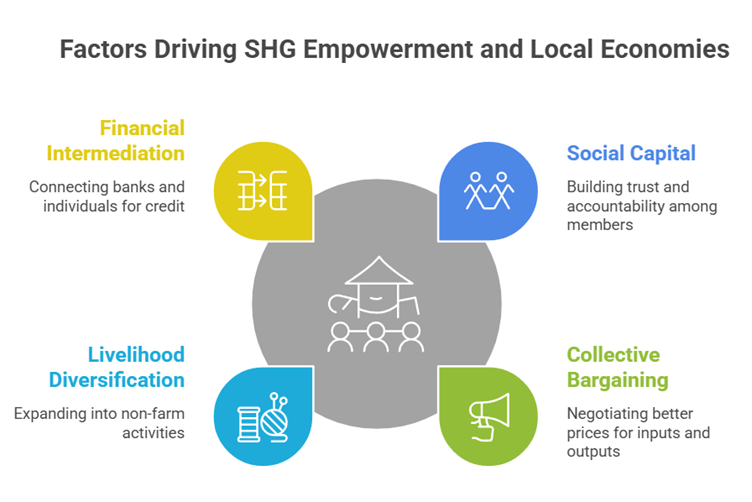

o 2.1 Social Capital Formation and Collective Bargaining Power

- SHGs promote peer learning, mutual accountability, and financial discipline, strengthening social cohesion and trust within communities.

- Collective bargaining has enabled women to negotiate better prices for inputs and outputs, improving profit margins.

- Case Study: Kudumbashree Mission (Kerala) has transformed women into micro-entrepreneurs, managing enterprises ranging from catering to waste management.

o 2.2 Livelihood Diversification and Rural Industrialization

- SHGs facilitate diversification into non-farm activities such as handicrafts, agro-processing, and services, reducing dependence on agriculture.

- This has led to localized value chains, boosting rural industrialization and employment generation.

- Example: In Bihar’s JEEViKA model, SHGs have created producer groups in sectors like makhana processing and dairy, significantly increasing rural incomes.

o 2.3 Financial Intermediation and Credit Linkages

- SHGs act as intermediaries between banks and individuals, ensuring credit absorption capacity and minimizing default risks.

- The SHG-Bank Linkage Programme (NABARD) has emerged as one of the world’s largest microfinance initiatives, with high repayment rates.

- Case Study: In Andhra Pradesh, SHG federations have successfully accessed large-scale institutional credit, enabling community-level investments.

3. Multiplier Effect: Socio-Economic Transformation Beyond Income

o 3.1 Women Empowerment and Human Development Outcomes

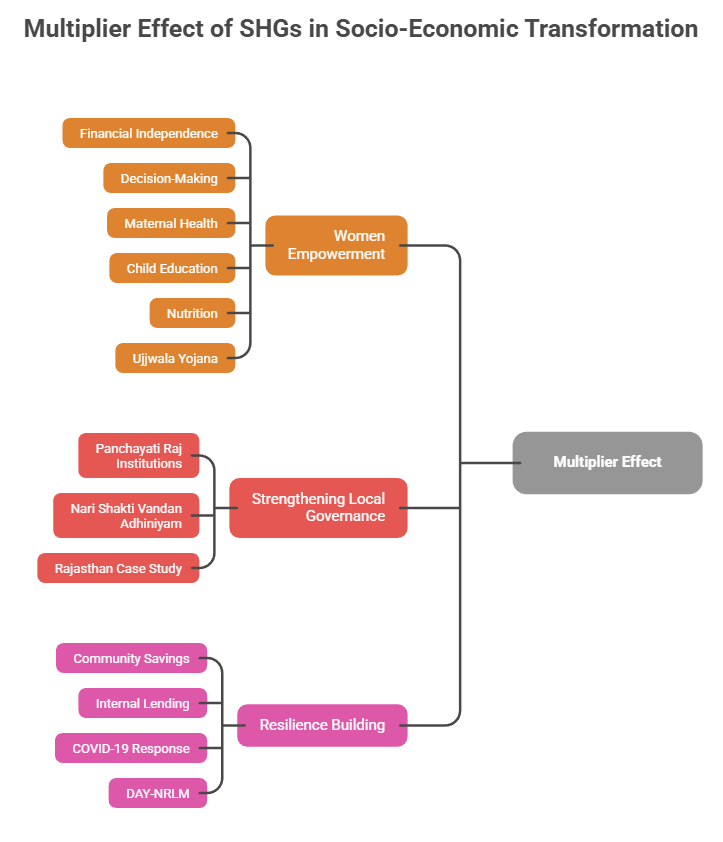

- Financial independence through SHGs has enhanced women’s participation in decision-making, mobility, and leadership roles.

- This translates into improved outcomes in maternal health, child education, and nutrition, creating intergenerational benefits.

- Example: The Ujjwala Yojana has reduced time spent on fuel collection, allowing women to engage in productive activities.

o 3.2 Strengthening Local Governance and Institutional Participation

- Financially empowered women are more likely to participate in Panchayati Raj Institutions, strengthening grassroots governance.

- The Nari Shakti Vandan Adhiniyam is expected to deepen this impact by increasing women’s legislative representation, aligning policy with ground realities.

- Case Study: Women SHG leaders in Rajasthan have transitioned into elected representatives, influencing local development priorities.

o 3.3 Resilience Building and Shock Absorption Capacity

- SHGs provide a safety net during crises through community savings and internal lending, enhancing resilience against shocks like pandemics or crop failures.

- During COVID-19, SHGs played a crucial role in producing masks, sanitizers, and ensuring food security.

- Example: Under DAY-NRLM, SHGs supplied essential goods, demonstrating their capacity as community institutions during emergencies.

Conclusion:

- The convergence of financial inclusion and the SHG movement has generated a powerful multiplier effect by transforming access into agency and participation into productivity. Evidence shows that regions with strong SHG networks and financial penetration exhibit higher rural incomes, better human development indicators, and stronger local governance outcomes. However, the next phase requires moving from account ownership to active usage, ensuring credit deepening, digital literacy, and institutional capacity building.

- Going forward, achieving universal saturation, strengthening last-mile delivery, and investing in women-led leadership ecosystems will be critical. If effectively implemented, this model can significantly contribute to India’s aspiration of becoming a $5 trillion economy while ensuring that growth remains inclusive, resilient, and sustainable.