De-dollarisation Implications for Global Financial Architecture: China and India’s Strategic Shift

De-dollarisation implications have become a central theme in debates on the future of the global financial architecture. As countries like China and India experiment with reducing reliance on the U.S. dollar in trade, finance, and reserves, the long-standing dollar-centric system is witnessing cautious but significant adjustments.

Introduction

De-dollarisation refers to the gradual reduction in reliance on the U.S. dollar for international trade, finance, and reserve holdings. For over seven decades, the dollar’s dominance—reinforced by oil pricing in dollars, deep U.S. financial markets, and geopolitical power—has anchored the global financial architecture. However, recent shocks have accelerated reassessment.

Sanctions regimes after 2014 and especially post-2022, rising geopolitical fragmentation, and the emergence of alternative payment and settlement mechanisms have coincided with major economies such as China and India experimenting with non-dollar trade, particularly in energy. These shifts carry systemic implications for currency hierarchies, capital flows, monetary sovereignty, and global governance, making de-dollarisation a critical issue for contemporary international political economy.

Body

I. Impact on Global Currency and Reserve Architecture

Gradual diversification of reserve portfolios

- Large economies have incrementally increased holdings of non-dollar assets, including gold and regional currencies, to hedge against geopolitical and sanctions-related risks. This has reduced the dollar’s uncontested centrality without displacing it as the primary reserve currency.

- Example: Central bank gold accumulation—China and several emerging economies have expanded gold reserves alongside modest diversification into non-dollar currencies, reflecting a search for financial insulation rather than outright confrontation.

Enhanced international role of alternative currencies

- China’s promotion of the yuan in bilateral trade, especially in energy and commodities, has strengthened its cross-border usage and encouraged experimentation with currency swap lines and clearing banks.

- Case Study: Yuan-based energy trade—Settlements for a portion of crude oil and gas imports through yuan-denominated contracts have marginally expanded the currency’s footprint in global trade.

Resilience yet relative dilution of dollar dominance

- While the dollar remains dominant due to liquidity, depth of U.S. capital markets, and investor confidence, its share in reserves and settlements has faced incremental erosion, suggesting a shift from a unipolar to a more plural currency order.

- Example: Post-sanctions adjustments—Sanctions on Russia accelerated diversification efforts among non-Western economies seeking to avoid vulnerability to unilateral financial coercion.

II. Transformation of Trade, Energy, and Payment Systems

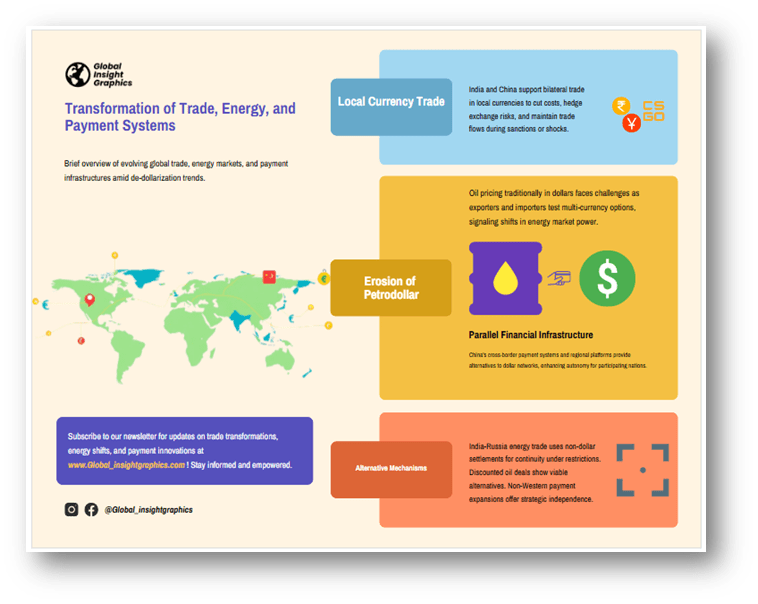

Local currency trade and alternative settlement mechanisms

- India and China have supported bilateral trade settlements in local currencies to reduce transaction costs, manage exchange-rate risks, and ensure continuity of trade under sanctions or supply shocks.

- Example: India–Russia trade arrangements—Partial settlement of energy imports using non-dollar currencies enabled trade continuity despite restrictions on dollar-based transactions.

Erosion of the traditional petrodollar system

- The long-standing practice of pricing oil exclusively in dollars is being cautiously challenged as some exporters and importers explore multi-currency invoicing, reflecting changing power dynamics in energy markets.

- Case Study: Energy trade diversification—Discounted crude purchases settled outside the dollar system have demonstrated functional, though limited, alternatives to dollar invoicing.

Rise of parallel financial infrastructure

- China’s development of cross-border payment systems and regional financial platforms offers redundancy to dollar-centric networks, reducing overdependence on a single clearing mechanism.

- Example: Alternative payment networks—Expansion of non-Western messaging and settlement platforms has provided strategic autonomy to participating states.

III. Strategic, Geopolitical, and Developmental Implications

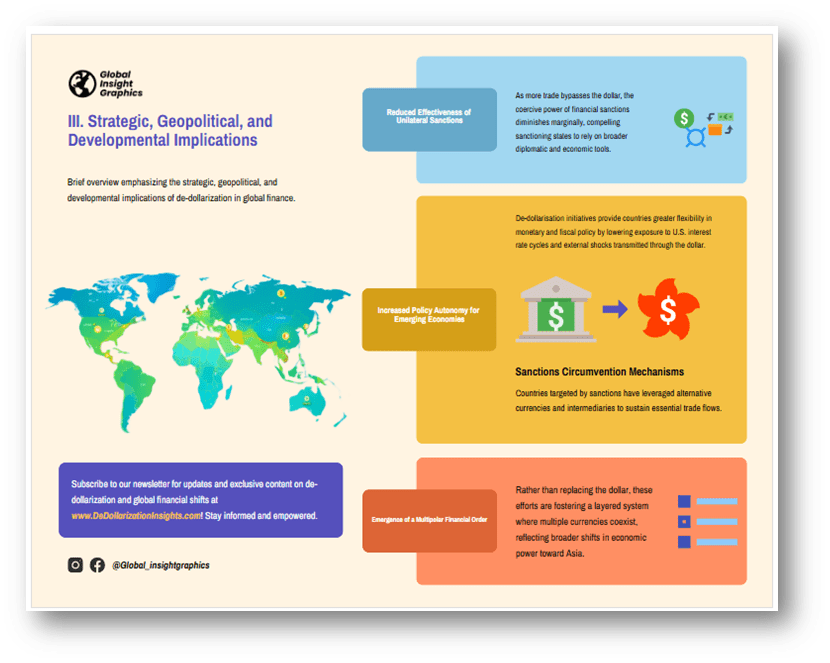

Reduced effectiveness of unilateral sanctions

- As more trade bypasses the dollar, the coercive power of financial sanctions diminishes marginally, compelling sanctioning states to rely on broader diplomatic and economic tools.

- Example: Sanctions circumvention mechanisms—Countries targeted by sanctions have leveraged alternative currencies and intermediaries to sustain essential trade flows.

Increased policy autonomy for emerging economies

- De-dollarisation initiatives provide countries greater flexibility in monetary and fiscal policy by lowering exposure to U.S. interest rate cycles and external shocks transmitted through the dollar.

- Case Study: Monetary insulation strategies—Local currency settlements have helped reduce balance-of-payments stress during periods of global tightening.

Emergence of a multipolar financial order

- Rather than replacing the dollar, these efforts are fostering a layered system where multiple currencies coexist, reflecting broader shifts in economic power toward Asia.

- Example: BRICS financial coordination—Discussions on shared settlement frameworks illustrate aspirations for collective resilience without immediate currency unification.

Conclusion

De-dollarisation driven by China, India, and other economies does not signal an imminent collapse of the dollar-based system, but rather a transition towards a more plural, multi-currency global financial architecture. The dollar’s dominance endures due to trust, liquidity, and institutional depth, yet its uncontested primacy is gradually giving way to selective diversification shaped by geopolitics, energy transitions, and technological change.

For the global economy, this evolution offers greater resilience and policy autonomy, but also raises coordination and stability challenges. The way forward lies in strengthening multilateral financial governance, reforming international institutions to reflect contemporary economic realities, and ensuring that currency diversification complements—rather than fragments—the global trading system.

For India, a calibrated approach that balances innovation with stability will be crucial in navigating this historic transition while safeguarding growth and strategic autonomy.

Recap: