Universal Basic Income (UBI) in India: Streamlining Welfare Delivery and Ensuring Inclusive Growth

Universal Basic Income (UBI) in India is gaining traction as a potential game-changer in social welfare and inclusive growth. A Universal Basic Income (UBI) is a policy model whereby every citizen receives a periodic, unconditional cash transfer, irrespective of employment status or income level. In the Indian context, such a scheme gains urgency given the stark inequality and welfare delivery challenges: for example, wealth-based estimates suggest the top 1% of India’s population owns about 40% of national wealth, with the top 10% holding nearly 65% or more. At the same time, India’s welfare architecture remains highly fragmented and prone to leakages. The question therefore is: can a UBI help streamline this system while promoting inclusive growth?

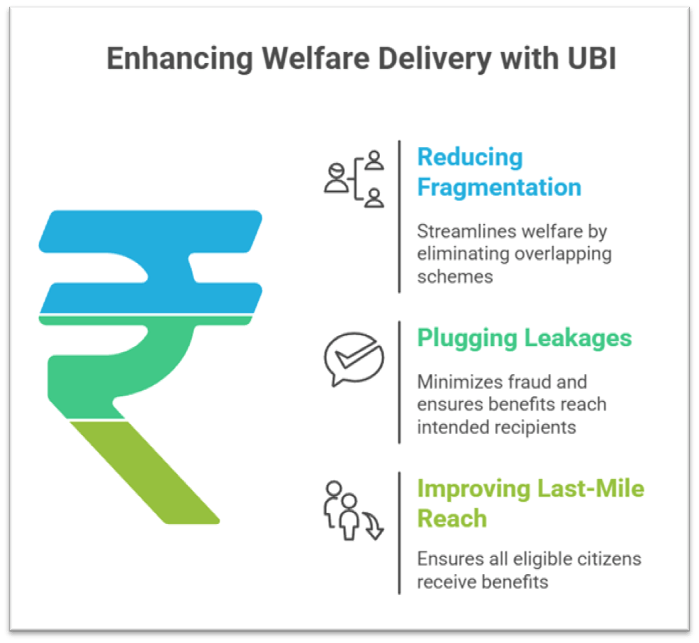

I. Streamlining Welfare Delivery

1. Reducing fragmentation and administrative complexity

India’s welfare system currently comprises a vast array of schemes across central and state levels with overlapping objectives and eligibility criteria. A UBI offers a single, unconditional transfer, thereby simplifying the delivery mechanism. The existing platform of Direct Benefit Transfers (DBT) shows what standardisation and digitisation can achieve: India’s DBT system has reportedly led to cumulative savings of about ₹3.48 lakh crore from 2009–24, and the subsidy share of total expenditure fell from about 16% to 9%. With a UBI, the government could bypass the many filters, exclusions, and means-tests associated with individual welfare schemes, reducing both costs and exclusion errors.

2. Plugging leakages and improving transparency

Traditional welfare delivery via in-kind subsidies and multiple intermediaries suffers from ghost beneficiaries, duplications and benefit capture by non-eligible individuals. A UBI, delivered directly into bank accounts, leans on existing digital infrastructure (for example, Aadhaar, Jan Dhan bank accounts) and so can reduce such leakages. Evidence from India’s DBT system suggests that leveraging Aadhaar and bank-linking significantly reduced ghost entries and duplication. Hence, a UBI can potentially further enhance transparency and accountability in welfare delivery.

3. Improving last-mile reach and universality

One of the most vexing problems in Indian welfare is exclusion of eligible beneficiaries due to complex eligibility criteria, poor identification, or bureaucratic bottlenecks. A UBI by being universal and unconditional removes eligibility filters and aims to include all citizens without separate verification of need. For example, pilot UBI experiments in India (such as by the Self-Employed Women’s Association (SEWA) and in Madhya Pradesh) found uptake and increased school attendance and nutrition outcomes, even among informal workers. Thus, the universal design of UBI presents a streamlined alternative to multiple overlapping schemes and promises fuller coverage.

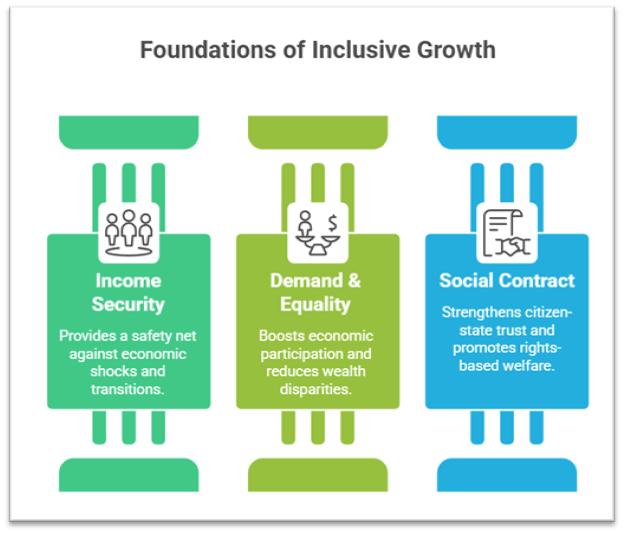

II. Promoting Inclusive Growth

1. Cushion against automation, informal sector risks and structural change

India faces increasing risks from automation, gig-economy precarity, climate shocks and informal employment. A UBI provides a floor of income security, giving workers more flexibility to transition, upskill, or respond to shocks. Given the informal workforce in India is large and unprotected, and structural inequality is rising (for instance, the median income of the top 1% grew much faster than that of the bottom 50%). Thus, by giving every citizen a basic income floor, UBI helps ensure no one is left behind in structural change and growth transitions.

2. Boosting demand, reducing inequality and empowering citizens

A UBI has the potential to expand aggregate demand by ensuring every household has some income security, thereby broadening the base of economic participation rather than concentrating growth benefits at the top. Given India’s wealth and income disparities, where the top 1% own disproportionate shares, a UBI can help redistribute purchasing power and therefore support more inclusive growth. Moreover, unconditional income helps support unpaid care work (predominantly by women), thus recognising non-market labour that currently goes unsupported and enabling greater gender equity.

3. Strengthening social contract and citizenship rights

By decoupling welfare from conditionality or employment-linked eligibility, UBI shifts the citizen-state relationship from one of patronage (you receive if you qualify) to a rights-based model (every citizen receives). This rights-based approach fosters dignity, autonomy and agency, enabling citizens to make choices rather than being passive recipients of welfare. In the Indian democracy, with rising insecurity, job-shedding and informalisation, a UBI could help stabilise livelihoods and thereby reinforce trust in the social contract—a pre-condition for inclusive growth.

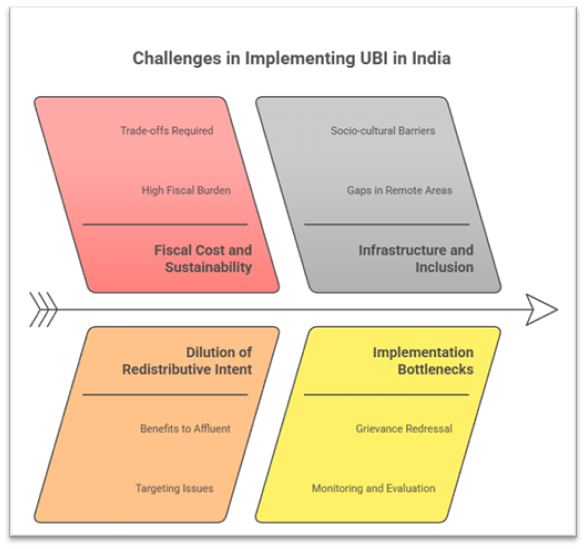

III. Practical Implementation Challenges & Governance Issues

1. Fiscal cost and sustainability

A major challenge of UBI in India is the fiscal burden. Estimates suggest that providing even a modest UBI (for example around the poverty line) would cost about 3–5% of GDP. Ensuring fiscal sustainability would require tough trade-offs: either raising taxes, cutting subsidies elsewhere, or increasing borrowing; each has implications for growth, macro stability and inter-generational equity.

2. Risk of dilution of redistributive intent and targeting issues

Because a universal scheme grants benefits to all, including affluent segments, it may dilute the redistributive impact unless financed via progressive taxation or accompanied by subsidy rationalisation. In a diverse country such as India, the question also arises whether a UBI should replace or complement existing targeted schemes (e.g., the Mahatma Gandhi National Rural Employment Guarantee Act (MGNREGA), PDS) in the interim, to preserve targeted support where needed.

3. Infrastructure, inclusion and implementation bottlenecks

While India has made progress via the JAM trinity (Jan Dhan, Aadhaar, mobile connectivity), gaps remain in remote and tribal areas: banking access, digital literacy, biometric failures, and socio-cultural barriers persist. Moreover, a universal scheme requires robust grievance redressal, monitoring and evaluation, and mechanisms to deal with inflation-driven behavioural responses (though empirical evidence suggests such risks are manageable). Pilot projects highlight operational challenges: for instance, the UBI pilot in Madhya Pradesh found improved outcomes but also emphasised the need for financial inclusion and banking access.

Conclusion:

The potential of Universal Basic Income (UBI) in India to streamline fragmented welfare delivery and foster more inclusive growth is significant. By reducing administrative complexity, plugging leakages, and offering a rights-based income floor, a UBI aligns with the imperatives of the 21st-century welfare state. However, its implementation must be carefully designed: phased roll-out, credible funding pathways, strong digital and financial inclusion infrastructure, and complementary schemes to address specific vulnerabilities.

Recap: