How China’s Rare Earth Dominance Threatens India’s Strategic Autonomy

Strategic autonomy refers to a nation’s ability to pursue its national interests and make sovereign decisions without being overly dependent on external powers for critical technologies, resources, or policy directions. For a country like India, aspiring to emerge as a major global manufacturing hub under initiatives like "Make in India", strategic autonomy is not merely desirable—it is essential for economic security, technological self-reliance, and geopolitical resilience.

However, China’s entrenched dominance in global supply chains and rare earth materials presents significant obstacles. According to the U.S. Geological Survey (2024), China controls over 60% of global rare earth production and nearly 90% of processing capabilities, making it the single largest source of inputs essential for electronics, green energy, and defence systems. This asymmetry fundamentally challenges India's ambitions to be Atmanirbhar (self-reliant), particularly in high-technology and critical manufacturing domains.

China’s Dominance in Rare Earths and its Strategic Leverage

- Control over Extraction, Processing and Export

- Production Monopoly: China produces around 210,000 tonnes of rare earth elements annually (USGS 2024), including neodymium, dysprosium, and terbium.

- Processing Bottlenecks: Other nations may have reserves, but China dominates refining and separation processes.

- Export Restrictions: In 2023 and 2024, China restricted exports of gallium, germanium, and graphite.

- Example: India’s delay in indigenous lithium-ion battery development is tied to reliance on Chinese imports.

- Embeddedness in High-Tech Manufacturing Chains

- Critical Minerals Cartel: China supplies components for telecom, EVs, and defence tech.

- Price Manipulation Strategy: Firms like BYD undercut competition by overproducing.

- Informal Trade Barriers: India faces shipment delays and bans from Chinese vendors.

- Export-Oriented Geoeconomics

- Export Revenue Dependency: China leans on export-led growth due to declining domestic demand.

- Weaponisation of Trade: Example: withdrawal of 300 Chinese engineers from Foxconn’s iPhone 17 unit in India.

- Manipulation of Human Capital

- China limits outbound technology expertise and issues administrative recalls.

- Example: Impact on electronics hubs in Tamil Nadu and Karnataka.

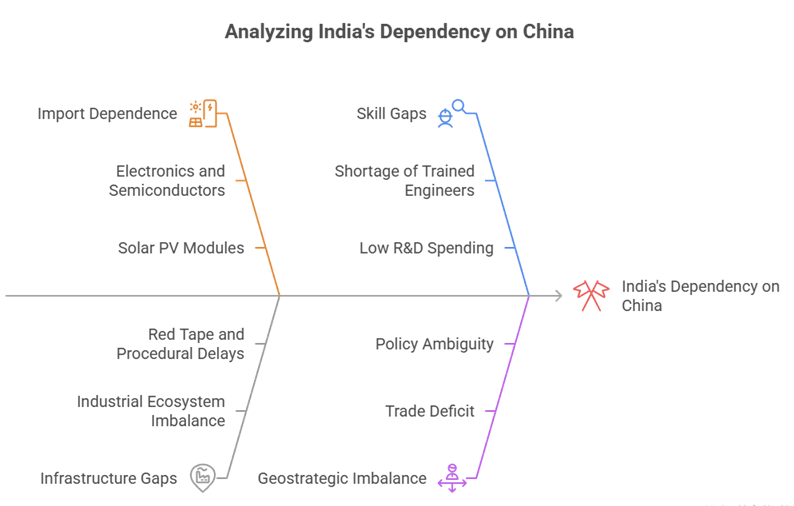

India’s Vulnerabilities and Dependency on China

- Import Dependence

- 80% of electronics component imports from China.

- 90% of solar modules are Chinese-made.

- 70% of APIs in the pharma sector are Chinese-origin.

- Infrastructure and Logistics Gaps

- Manufacturing clusters lack Shenzhen-style integration.

- Slow land allocation and red tape hinder execution.

- Example: Micron plant in Gujarat still imports all machinery.

- Skill Gaps and Tech Lag

- Shortage of engineers in nanotech and precision electronics.

- India’s R&D spending is 0.65% of GDP vs China’s 2.4%.

- Geostrategic Imbalance

- Trade deficit with China crossed USD 100 billion in FY2024.

- Friend-shoring policies remain unreliable.

- India not part of US-led Minerals Security Partnership (MSP).

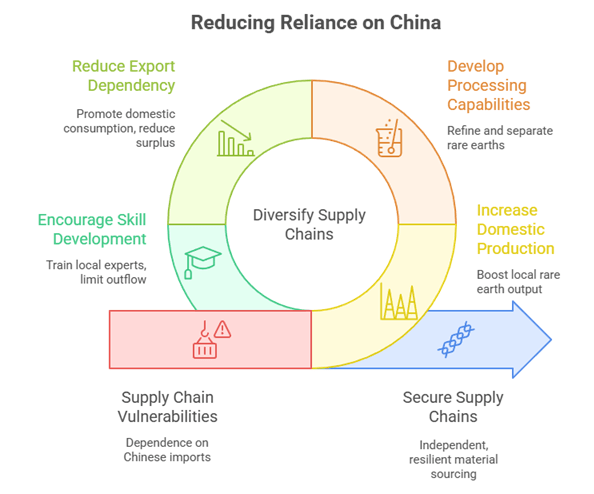

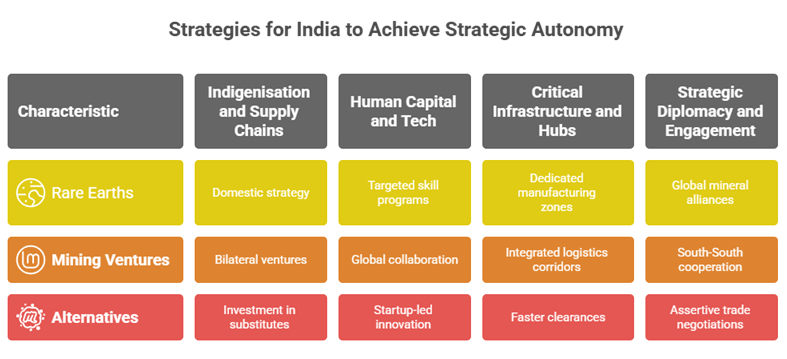

Strategies for India to Achieve Strategic Autonomy

- Indigenisation and Supply Chain Diversification

- India has 6% of global rare earth reserves—must be exploited by IREL (India) Ltd.

- Form MOUs with Australia, Vietnam, and Africa for joint processing.

- Example: India-Vietnam agreement (2022) for Dong Pao rare earths.

- Human Capital and Technology Ecosystem

- Skill programs like SANKALP and FutureSkills PRIME must integrate fab tech.

- Partnerships with Japan, Israel to boost R&D.

- Startup push: India Semiconductor Mission, C2S (Chips to Startup).

- Infrastructure and Industrial Hubs

- Develop Yadadri and Dholera as plug-and-play hubs.

- Integrate with PM Gati Shakti and National Logistics Policy.

- Fast-track SOPs for investment clearance.

- Strategic Diplomacy

- Join global mineral alliances like Critical Minerals International Partnership.

- South-South cooperation for joint mining in Africa and Latin America.

- Example: India’s LITHIUM JV in Argentina via KABIL.

Conclusion:

India’s quest for strategic autonomy is a long-haul journey. China’s dominance in rare earths and critical supply chains presents both a challenge and a wake-up call. This is not just about economics—it’s about sovereignty.

India must systematically address internal gaps, strengthen its manufacturing ecosystems, and build multilateral partnerships to truly become Atmanirbhar in a multipolar world. With rising FDI and global interest in India, the opportunity exists—if matched with strategic intent and execution.

Recap: