Institutional and Administrative Bottlenecks in Urban Local Bodies: Why ULBs Struggle to Leverage Municipal Bonds and Private Capital

Institutional and Administrative Bottlenecks in Urban Local Bodies significantly limit their ability to leverage municipal bonds and private capital effectively. Urban Local Bodies (ULBs) are constitutionally recognised institutions of self-government entrusted with providing essential urban services such as water supply, sanitation, housing, and infrastructure, following the 74th Constitutional Amendment Act, 1992, which sought to promote fiscal decentralisation, administrative autonomy, and democratic accountability.

However, India’s rapid urbanisation—with urban population projected to reach over 600 million by 2036 contributing nearly 70% of GDP—has sharply increased infrastructure demands estimated at over $840 billion, far exceeding traditional public funding.

This has led to a growing emphasis on market-based financing mechanisms such as municipal bonds, loans, and Public-Private Partnerships (PPPs). Yet, structural issues related to weak fiscal autonomy, inadequate revenue generation, and limited administrative capacity constrain ULBs’ ability to access and effectively utilise such financing.

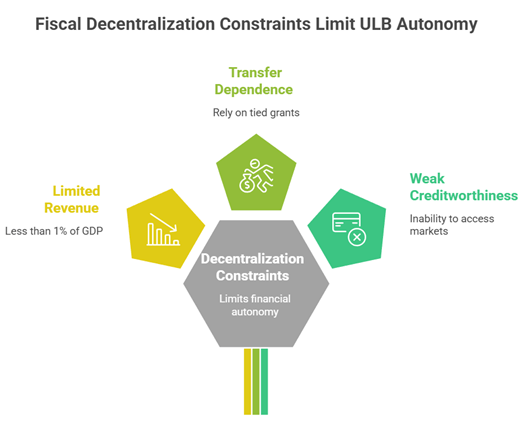

Fiscal Decentralisation Constraints Limiting Financial Autonomy

1. Limited Revenue-Raising Powers and Vertical Fiscal Imbalance

- Despite constitutional recognition, ULBs account for less than 1% of GDP in revenue, compared to 6–7% in OECD countries, reflecting weak fiscal decentralisation and dependence on State and Central transfers.

- Key taxes such as property tax, stamp duty, and user charges are either restricted by State governments or suffer from poor assessment and collection efficiency, reducing financial credibility.

- Example: Property tax inefficiencies in Indian cities—collection efficiency remains around 0.15% of GDP, far below global benchmarks, reducing ULBs’ ability to generate predictable revenue streams required for borrowing.

2. Dependence on Intergovernmental Transfers and Conditional Funding

- ULB finances heavily rely on tied grants under schemes such as AMRUT, Swachh Bharat Mission Urban 2.0, Smart Cities Mission, and Pradhan Mantri Awas Yojana (Urban), limiting financial flexibility.

- Conditional funding structures prioritise compliance over local needs, preventing ULBs from independently leveraging finances based on local priorities.

- Example: Delays in PMAY(U) implementation—many cities faced funding delays and incomplete housing projects, demonstrating structural dependence on higher-level fiscal transfers.

3. Weak Creditworthiness and Inability to Access Financial Markets

- Market-based financing depends on credit ratings, predictable revenue flows, and debt servicing capacity, which most ULBs lack due to unstable fiscal bases.

- The introduction of instruments like the Urban Challenge Fund, which requires cities to raise 50% of funds through market instruments, highlights systemic inequities as financially weaker cities lack borrowing capacity.

- Example: Municipal bond success limited to few cities—Pune, Ahmedabad, and Indore have successfully issued bonds due to strong revenue bases, while most smaller cities remain excluded.

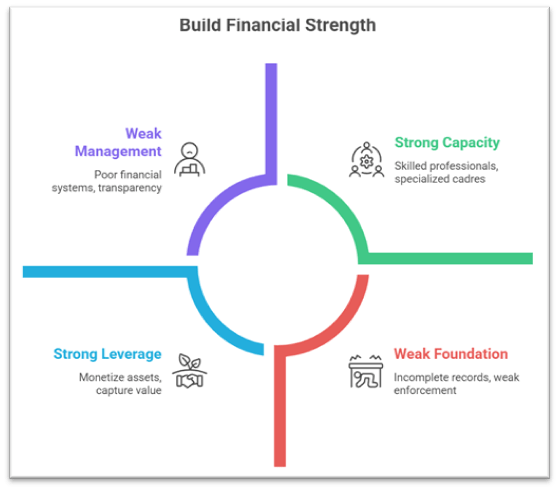

Administrative and Institutional Capacity Constraints Affecting Financial Viability

1. Weak Financial Management, Accounting, and Transparency Systems

- Many ULBs lack modern accrual-based accounting, financial disclosure systems, and asset registers, undermining investor confidence and increasing perceived credit risk.

- Weak financial governance creates risks of misallocation, inefficiencies, and poor monitoring of infrastructure investments.

- Example: Audit findings under Ujwal DISCOM Assurance Yojana (UDAY) revealed significant implementation gaps and accounting inconsistencies.

2. Limited Technical Expertise and Institutional Manpower

- ULBs face shortages of trained professionals in urban planning, project structuring, financial engineering, and contract management.

- Administrative structures remain dominated by generalist bureaucracies rather than specialised municipal cadres.

- Example: Capacity-building gaps under Smart Cities Mission—large cities like Surat progressed faster than smaller cities.

3. Incomplete Land Records and Regulatory Weaknesses Affecting Asset Monetisation

- Reliable land ownership records are essential for leveraging land-based financing tools such as land value capture and leasing.

- Violations of master plans and weak enforcement reduce predictability and investor confidence.

- Example: Poor digitalisation and unclear titles have limited infrastructure financing potential in Indian cities.

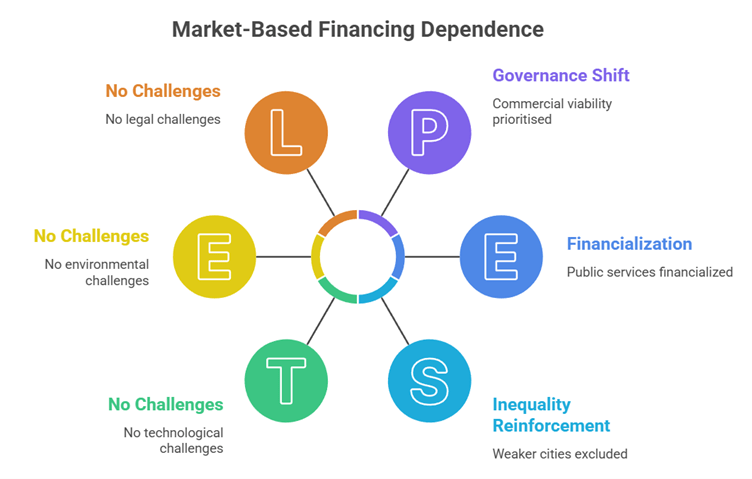

Structural Risks and Inequities Associated with Market-Based Financing Dependence

1. Risk of Excluding Weaker Cities and Reinforcing Urban Inequality

- Market financing favours financially strong cities, leaving smaller and poorer cities dependent on uncertain grants.

- This creates a two-tier urban system with uneven infrastructure development.

- Example: Over 80% of bond financing has been limited to a few large cities such as Pune and Ahmedabad.

2. Shift in Governance Priorities Towards Commercially Viable Projects

- Market-linked financing encourages investments in commercially profitable infrastructure rather than essential public services.

- This risks neglecting vulnerable populations and low-income communities.

- Example: PPP housing projects often prioritise revenue-generating developments.

3. Increasing Financialization of Public Services and Fiscal Risk Exposure

- Reliance on borrowing exposes ULBs to debt sustainability risks and financial instability.

- Similar patterns are visible in other public sectors facing funding pressures.

- Example: Delays under the National Health Mission illustrate risks of unstable financing mechanisms.

Conclusion:

India’s urban transformation requires strong, financially empowered ULBs capable of mobilising diverse funding sources while ensuring equitable service delivery. While market-based financing instruments such as municipal bonds and PPPs are important, they cannot substitute the fundamental need for deep fiscal decentralisation, predictable transfers, and strengthened administrative capacity.

The 15th Finance Commission’s allocation of over ₹1.21 lakh crore to ULBs, along with reforms such as GIS-based property tax reforms, municipal cadre creation, credit enhancement mechanisms, and pooled financing models, can significantly improve fiscal autonomy and creditworthiness.

Strengthening institutional capacity alongside fiscal empowerment will ensure that market-based financing complements, rather than replaces, the core objective of inclusive, sustainable, and accountable urban governance.

Recap: