India-Australia Renewable Energy Partnership: Strategic Significance in Supply Chains & Critical Minerals

The India-Australia Renewable Energy Partnership (REP) constitutes a strategic bilateral framework aimed at deepening cooperation in the clean energy domain. At a time when the world is grappling with climate change, volatile supply chains, and geopolitical competition, this partnership acquires particular salience. The global clean energy transition depends heavily on critical minerals, solar components, batteries and hydrogen technologies, segments where supply chains are currently highly concentrated. In fact, China controls a significant share of midstream and downstream processing — e.g. processing 68 % of global nickel, 59 % of lithium, and large shares of battery components such as cathodes, anodes and separators. (e.g. China’s dominance in cathodes 70 %, anodes 85 %)¹ Such concentration translates into systemic vulnerabilities. The REP, by leveraging complementarities between India and Australia, offers a pathway to reduce dependency on a single country and build a more resilient, diversified clean energy ecosystem.

Addressing Supply Chain Vulnerabilities

1. Diversification of Critical Mineral Supply

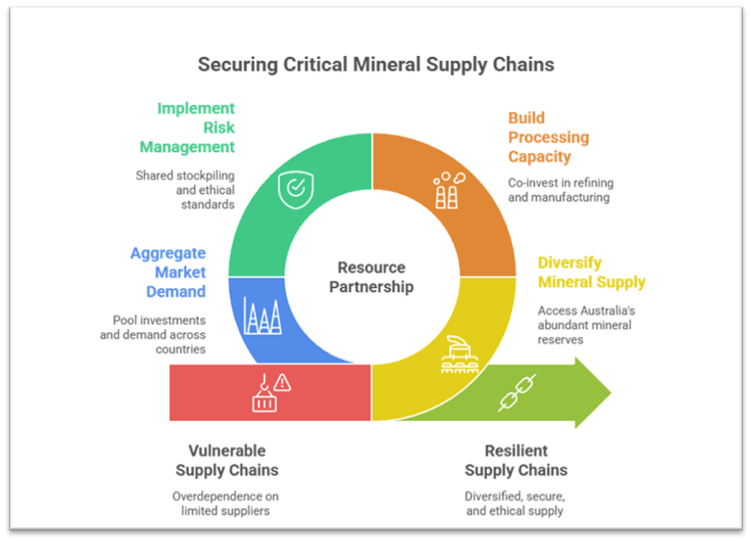

- Reducing import concentration risk: India currently relies heavily on imports of critical minerals (e.g. lithium, cobalt, rare earths) and suffers from overdependence on China and other limited suppliers. The REP provides a framework by which India can access Australia’s abundant reserves and integrate them into its value chains.

- Australia’s resource endowment and policy alignment: Australia is among the world’s leading producers of lithium and other minerals, and has enunciated a Critical Minerals Strategy (2023-2030) along with investment incentives under its Future Made in Australia agenda. India and Australia already cooperate under a Joint Working Group on critical minerals.

- Tripartite or corridor models: The REP allows for creation of a mineral corridor linking Australian mines to Indian processing hubs, thereby reducing intermediaries and transit vulnerabilities. This corridor model can also serve supply to other like-minded partners in the Indo-Pacific region.

2. Building Downstream Processing & Value Addition

- Avoiding the “raw-material exporter trap”: Australia, while rich in raw materials, currently lacks large-scale refining and downstream manufacturing. India has strengths in manufacturing scale, workforce, and policies (e.g. Production-Linked Incentive schemes). Under REP, co-investment in refining, separation, battery cell manufacturing etc. can capture more value within the bilateral domain.

- Technology and know-how transfer: The REP’s emphasis on solar PV, green hydrogen, energy storage, and circular economy enables the transfer of advanced processing technologies, catalyst development, battery chemistry R&D, and recycling techniques.

- Circular economy and recycling linkage: Processing of end-of-life batteries, reuse of rare earths, and waste valorisation (circular economy) is a stated pillar of REP. By building closed-loop industries, dependence on virgin supply and choke points can be mitigated.

3. Risk Management & Resilience

- Buffering against export controls or geopolitical disruption: In recent years, China has used export restrictions on rare earths (e.g. gallium, germanium, graphite) to exert leverage. A diversified supply chain under the REP acts as a hedge against such risks.

- Shared stockpiling and strategic reserves: India and Australia could coordinate strategic reserves of critical minerals for emergency release or to dampen price spikes. Such stockpiling is often part of resilience planning in essential commodities.

- Standards, traceability, and transparency: Through institutional cooperation, REP can institute traceability and ethical mining standards (e.g. sustainability, labour compliance) that enhance the credibility of bilateral supply. This prevents third-party disruptions from cascading across the chain.

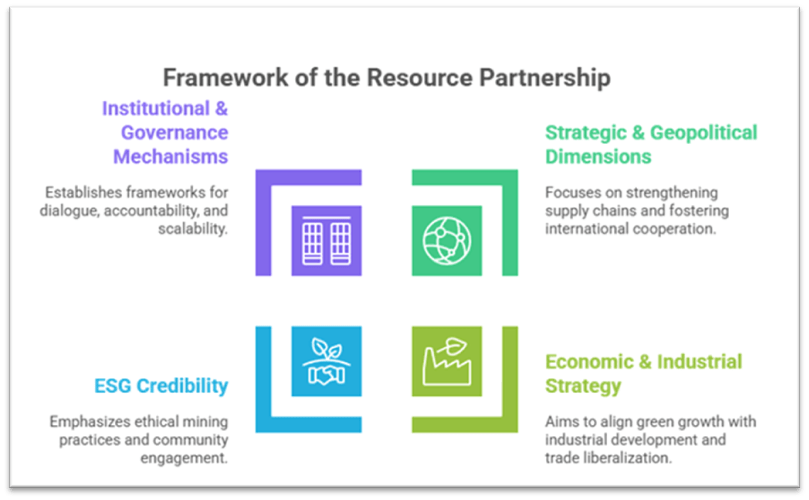

Strategic & Geopolitical Dimensions

1. Strengthening the Indo-Pacific Supply Architecture

- Anchoring supply chains within the democratic bloc: The REP helps consolidate supply chain nodes in India and Australia — democracies with rule-based institutions — thereby providing an attractive alternative to authoritarian-dominated chains.

- Catalysing multilateral cooperation: The REP model can serve as a prototype for wider cooperation with Japan, the U.S., ASEAN, Africa, and other resource-rich nations to create interlinked supply networks. India–Australia cooperation complements broader initiatives like the Mineral Security Partnership (MSP) among democracies.

- Geo-strategic deterrence through economic resilience: A more resilient supply architecture lowers the strategic leverage that any single country has over the energy transition in key states. This contributes to deterrence and strategic stability in the Indo-Pacific.

2. Economic & Industrial Strategy

- Linking green growth with industrial development: The REP aligns climate goals with industrial policy: India can attract Australian downstream investments, creating jobs and moving up the value chain; Australia can leverage India’s skilled workforce and manufacturing ecosystems.

- Trade and investment liberalisation support: The REP is nested within broader trade frameworks—such as India-Australia CECA/ECTA processes—and can benefit from preferential tariffs (e.g. removal of duties on key minerals).

- Technology-led competitiveness: Collaborative R&D, joint standards, and innovation under REP sharpen competitiveness in next-gen clean technologies (e.g. novel battery chemistries, hydrogen catalysts, advanced PV cells), thereby reducing vulnerability to technological lock-in by dominant players.

3. Environmental, Social and Governance (ESG) Credibility

- Ethical mining commitments: In a climate-sensitive era, the REP can enforce high standards for environmental, social, and governance practices in mining and processing — helping ensure that supply is not only resilient, but also sustainable.

- Community acceptance and social licence: Transparent cooperation, local employment, community engagement, and equitable benefit-sharing improve the legitimacy of mineral projects, minimizing social risk.

- Life-cycle emissions management: With joint oversight, India and Australia can coordinate emissions accounting, clean energy inputs in processing, and carbon footprint control — making their critical mineral outputs more attractive globally, especially in climate-aligned markets.

Practical Challenges & Enablers for Success

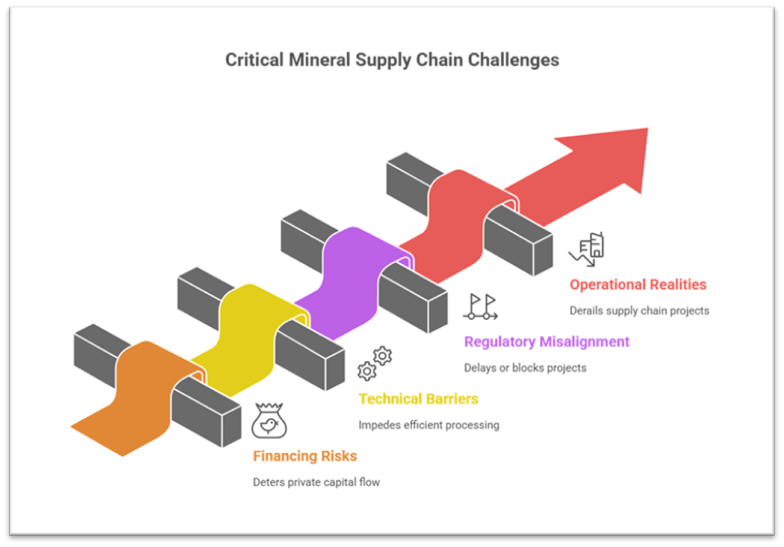

1. Financing & Investment Risk

- Capital-intensive nature and risk perceptions: Investments in mineral processing, battery manufacturing, and hydrogen infrastructure are capital-intensive and have long gestation. Risk perceptions around commodity volatility, regulatory changes, or project delays can deter private capital.

- De-risking mechanisms: Governments must deploy guarantees, blended finance, concessional capital, and off-take agreements to lower risks. For example, Australia has recently announced A$600 million support to sustain its copper refinery operations.

- Mobilising multilateral and institutional funds: Involvement of institutions like ADB, World Bank, climate funds, and sovereign wealth funds can crowd in private investments in sensitive segments of the supply chain.

2. Technical & Infrastructure Barriers

- Technology gaps and scaling challenges: Some critical-processing technologies (e.g. rare earth separation, advanced battery chemistry) require specialized expertise and scaling. Bridging these gaps demands robust R&D collaboration and talent exchange.

- Logistics, transport and supply connectivity: Efficient ports, transport corridors, power, water, and connectivity infrastructure are essential for linking mines to processing units. Investments into corridors and logistics (such as maritime, transshipment, customs) are needed.

- Standards, interoperability and certification: Aligning standards across two countries (e.g. for battery modules, hydrogen purity) is vital to avoid bottlenecks. Certification regimes and quality assurance must be harmonized.

3. Regulatory & Policy Alignment

- Harmonisation of mining, environmental and export policies: Divergent regulatory regimes (e.g. environmental reviews, land acquisition, export controls) can delay or block joint projects. Coordination, fast-track clearances, and mutual recognition are needed.

- Tariff and trade barriers: While some mineral tariffs have been removed under India-Australia trade arrangements, further tariff concessions, non-tariff barrier reduction, and regulatory alignment are required to support downstream flows.⁷

- Safeguards for national interest: Each country must ensure that critical projects do not compromise sovereignty, resource control, or strategic autonomy. Clear rules on ownership, equity participation, and exit must be defined.

4. Operational & Market Realities

- Demand uncertainty and price cycles: Minerals and batteries face volatile price cycles. Ensuring stable off-take commitment from Indian industry (e.g. EV, solar module makers) is crucial to provide demand certainty.

- Competition from existing supply chains: China and other players already enjoy scale and cost advantages; new bilateral supply chains must compete on cost, reliability and environmental credentials.

- Coordination across stakeholders: Success requires seamless coordination among ministries (energy, mines, commerce), state governments, industry, academia, and local communities. Misalignment or delays can derail projects.

Conclusion:

The India-Australia Renewable Energy Partnership (REP) embodies a strategic opportunity to reconfigure global clean energy supply chains away from excessive concentration and toward a more resilient, diversified architecture. By leveraging Australia’s resource endowments, India’s manufacturing scale, and shared democratic values, the REP can mitigate vulnerabilities, strengthen the Indo-Pacific supply base, and contribute to geopolitical stability.

If implemented effectively, REP can become a beacon of strategic autonomy in the green era, reducing dependence on single-country dominance, and ensuring that India, Australia and their partners benefit from resilient, sustainable clean energy value chains.

Recap: