GST Slab Simplification and Inverted Duty Structure Correction: Impact on India’s Manufacturing and Export Competitiveness

Introduction

On September 2025, during its 56th meeting, the GST Council introduced a sweeping reform—transitioning from four GST slabs (5%, 12%, 18%, 28%) into a simplified structure with two principal rates: a Merit Rate of 5% and a Standard Rate of 18%, plus a 40% rate for sin/luxury goods. These changes, effective from 22 September 2025, mark a pivotal shift toward GST slab simplification, aiming at greater simplicity, fairness, and economic stimulus.

The reform is designed to simplify compliance, reduce litigation, bolster consumption, and enhance international competitiveness—especially for manufacturing and exports. Policymakers project a net revenue loss of around ₹48,000 crore, expected to be offset by improved demand and compliance.

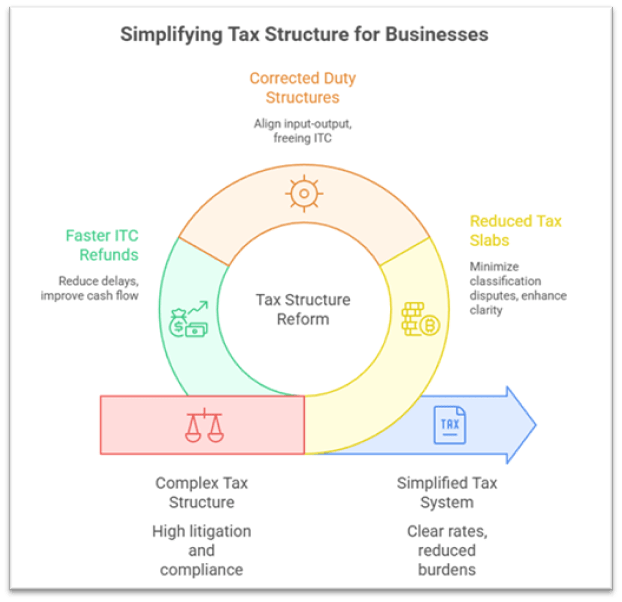

1. Structural Simplification

- Reduced Complexity & Litigation: Transition to two main slabs minimizes classification disputes and enhances clarity for exporters and manufacturers. Textile exporters previously tangled in classifications now benefit from reduced administrative burdens.

- Improved Input Tax Credit (ITC) Flow: The new framework corrects inverted duty structures, especially in textiles, auto parts, and electronics. Example: Man-made fibre/yarn rates reduced from 18%/12% to 5%, aligning input-output.

- Cash Flow & Working Capital Relief: Companies face fewer ITC refund delays, though industrial hubs like Ludhiana still struggle with refund timelines.

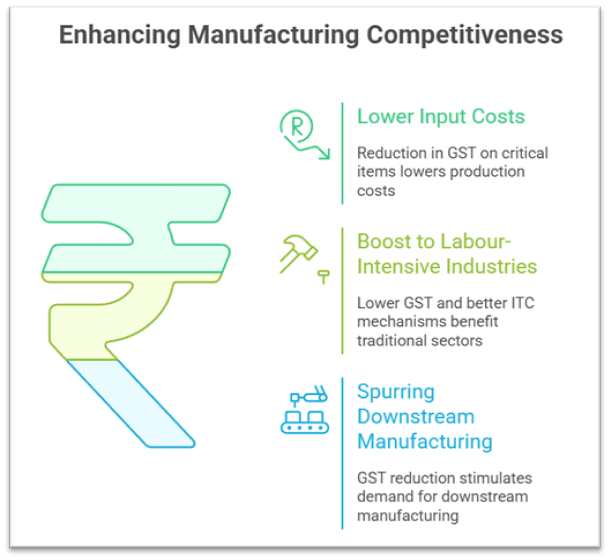

2. Manufacturing Competitiveness

- Lower Input Costs: Reduction in GST on automobile parts, farm machinery, and bio-pesticides lowers production costs and boosts domestic manufacturing.

- Boost to Labour-Intensive Industries: Handicrafts, textiles, and leather goods benefit from rationalised GST and better ITC mechanisms.

- Spurring Downstream Manufacturing: Reduction in GST on cement, electronics, and autos stimulates demand in construction and consumer durables.

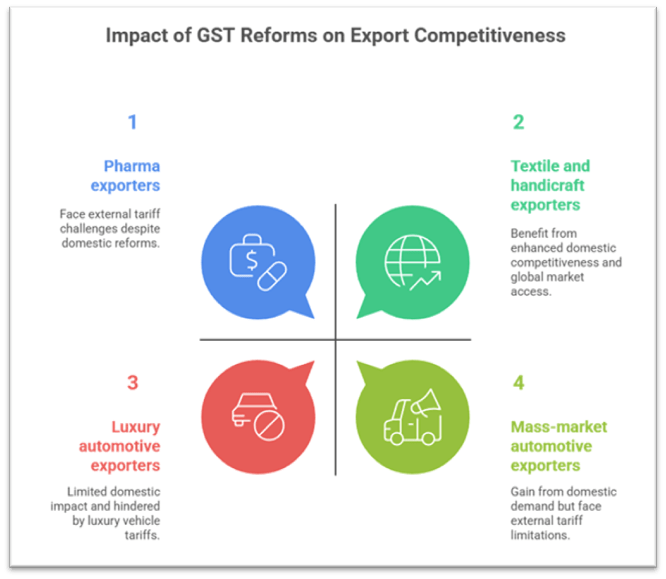

3. Export Competitiveness

- Indirect Gains: Though GST is not levied on exports, improved domestic competitiveness strengthens export readiness.

- Limits: GST reforms cannot offset external tariff barriers like U.S. duties on pharma or gems.

- Sectoral Gains: Textile and handicraft exporters benefit, while luxury vehicle exports may suffer due to the 40% slab.

- Market Response: Positive stock market reactions from auto and FMCG firms reflect optimism about competitiveness gains.

4. Critical Judgment

Strengths: Simplicity, better ITC flow, reduced costs, and improved demand. Weaknesses: Refund delays, revenue risks, external tariffs, and adverse impact on luxury segment exports.

Conclusion:

The reform represents a landmark shift toward a simpler, fairer, and growth-oriented GST regime. By pruning complexity and correcting distortions, GST slab simplification and inverted duty structure correction provide a strong foundation to enhance India’s manufacturing efficiency and export viability—provided complementary administrative safeguards are diligently implemented.