Introduction

- The recent GST reforms approved by the 56th GST Council on 3 September 2025 mark a watershed moment in India’s indirect tax architecture. At its core is the principle of simplifying and rationalising rates and reducing compliance burdens while correcting structural distortions.

- Under the new regime, the erstwhile four-rate structure (5 %, 12 %, 18 %, 28 %) has been largely replaced by a merit/low rate around 5 %, a standard rate at 18 %, and a de-merit/luxury rate at 40 % (for select “sin” and luxury goods).

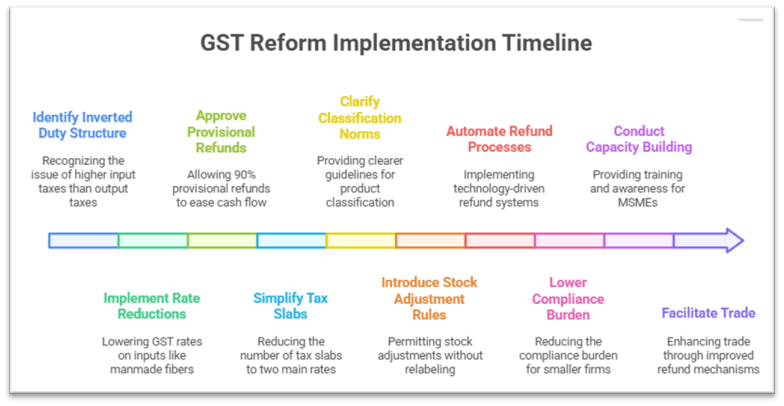

- Simultaneously, the Council has proposed procedural reforms—such as grant of 90 % provisional refunds in inverted duty cases, clearer classification norms, and easing of labelling/stock adjustments. These changes aim to address persistent grievances of industry (especially MSMEs), reduce litigation, and better integrate India’s manufacturing and export sectors with global value chains.

Body

I. Addressing Long-Standing Issues in the GST Regime

1. Tackling the Inverted Duty Structure

- Nature of inversion problem: Under the previous regime, many key inputs (plastics, chemicals, steel) faced 18 % GST, while their finished goods (such as toys, handicrafts, certain processed goods) were taxed at lower rates like 5 % or 12 %. This forced firms to seek refunds of accumulated input tax credits, creating cash flow constraints and procedural delays.

- Reforms to correct inversion: The 2025 reform reduces GST on many input-intensive sectors. For example, manmade fibre rates fall from 18 % to 5 %, and manmade yarn from 12 % to 5 %. Similarly, in the fertilizer sector, sulphuric acid, nitric acid, ammonia are moved from 18 % to 5 %, reducing inversion for fertilizer producers.

2. Reducing Litigation and Classification Disputes

- Simpler, fewer slabs reduce disputes: By collapsing multiple slabs into primarily two rates (5 % and 18 %), classification ambiguity is likely to decline. Many items earlier causing litigated disputes (e.g., whether a product is 12 % or 18 %) now will fall within clearer brackets.

- Clearer classification norms and explanations: The GST Council has recommended explicit clarifications (e.g., for restaurant services and “specified premises”) to reduce interpretational ambiguity.

- Transitional stock adjustment rules: The reforms permit stock adjustments without complete relabelling, easing the transition and reducing disputes over inventory held under old tax regimes.

- Faster refunds and process automation: The reforms envision automated refunds, risk-based scrutiny, and a more technology-driven backend, which will reduce discretionary decision-making and litigation triggers.

3. Improving Ease of Compliance & MSME Relief

- Lower compliance burden: Smaller firms, especially those with simpler supply chains, will benefit from the collapse of rate complexity, fewer rate revisions, and simplified return formats (e.g., pre-filled returns).

- Capacity building & outreach: The government and industry bodies (e.g., CII) commit to training and awareness for MSMEs, helping them adapt to classification, input credit flows, and procedural changes.

- Bridging transition costs: The government has signalled being sensitive to unsold inventory, labeling changes, packaging norms, and will maintain feedback loops to address residual anomalies.

4. Trade Facilitation & Refund Mechanisms

- Refunds for low-value exports: The Council recommended amendments to permit refunds even for low-value export consignments, enhancing export-friendliness.

- Risk-based scrutiny and provisional sanctioning: Refund claims (especially in inversion and zero-rate cases) will be subject to automated risk-assessment, allowing faster provisional disbursal and reducing delays.

- Valuation alignment & rules update: Changes in valuation rules (especially for lottery tickets and goods switching rate slabs) are being aligned to avoid inadvertent tax cascade.

Implications for India’s Manufacturing Competitiveness

1. Lower Input Costs & Enhanced Value Addition

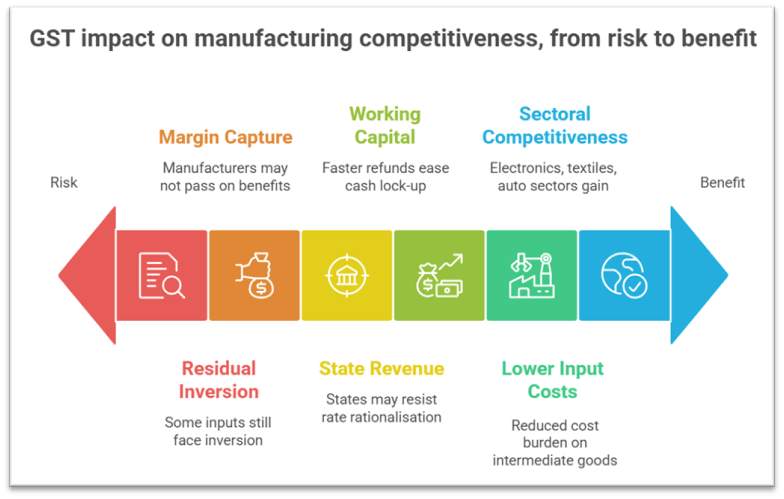

- Reduced cost burden on intermediate goods: With key raw materials and intermediate inputs coming under lower GST slabs, overall input cost for manufacturing will decline. For instance, the fall in GST on chemical inputs (in fertilizer) directly reduces cost in agricultural goods manufacturing.

- Better margin buffer for MSMEs: Smaller manufacturers, who often lack negotiating power, will benefit disproportionately from lower cost structures and improved working capital.

- Encouragement for backward integration: Lower taxation on upstream components will incentivize firms to internalise stages of production rather than outsource, fostering greater value addition domestically.

2. Reduction in Working Capital Blockage

- Faster refund mechanisms ease blockage: The 90 % provisional refund rule in inverted duty cases helps alleviate cash lock-up, enabling firms to reinvest working capital more fluidly.

- Less cumbersome classification disputes reduce delay: With fewer ambiguous classifications, fewer supply chain disruptions or audit holds arise, improving certainty in production planning.

- Improved predictability fosters investment: A more stable regime lowers risk premiums for new capacity expansion, especially capital-intensive manufacturing.

3. Potential Risks & Mitigation

- Residual inversion pockets: Some items (e.g. certain inputs for bicycles or corrugated boxes) may still face inversion, as flagged by industry. Timely reviews and corrective notifications will be necessary.

- Risk of margin capture upstream: Manufacturers may not always pass on benefits fully downstream; absence of revived anti-profiteering rules may limit enforcement.

- State-level revenue adjustments: States dependent on GST may resist further rate rationalisation, potentially slowing full adoption or leading to divergent implementation.

Export Competitiveness & External Sector Impacts

1. Strengthening India’s Export Value Chains

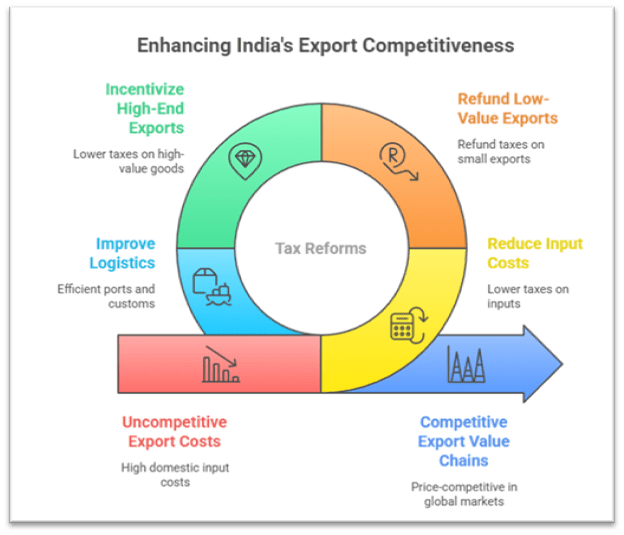

- Cost parity with global competitors: Reduced domestic input costs will make Indian exports more price-competitive in global markets, especially in textiles, leather goods, electronics.

- Greater forward-backward linkage: When domestic component sourcing becomes cheaper and reliable, exporters can build integrated value chains within India, reducing dependence on imports.

- Refunds for low-value exports expand reach: The facility for refund on low-value consignments will help micro exporters and e-commerce players compete in global digital markets.

2. Incentivising High-End Manufactured Exports

- Margin for differentiation: With lower input taxation, firms can allocate more to R&D, quality upgrades, branding, thereby moving up the export ladder from commodity to semi-processed or high-value goods.

- Encouraging export diversification: Sectors such as medical devices (lowered from 18 % to 5 %), electronics, and specialty chemicals can see new export potential.

3. Trade Balance and Revenue Dynamics

- Short-term revenue loss vs long term gains: The reforms may lead to initial loss in GST revenues (estimated in tens of thousands of crores) but may be offset over time via increased exports, formalisation, wider tax base, and higher compliance.

- Multiplier effect from consumption: The cut in rates is expected to inject demand and consumption (analysts project over ₹2 lakh crore boost), part of which may translate into greater demand for “Made in India” exports.

4. Challenges & Policy Actions Required

- Ensuring pass-through to exporters and global markets: Exporters must benefit from cost cuts and not be undermined by upstream price retention.

- Strengthening logistics and trade facilitation: Tax reform alone won’t suffice; efficient ports, customs clearance, compliance support systems critical for exports.

- Continuous review & feedback: Some inversion or classification mismatches may persist — fast-tracked review and sectoral consultations will be essential for course correction.

Conclusion

- The GST 2.0 reforms of September 2025 represent a bold attempt to resolve some of the most intractable structural distortions in India’s indirect tax system. By targeting inverted duty structure, classification ambiguity, compliance burden, and refund backlogs, the reforms address core pain points long raised by industry.

- For manufacturing, the anticipated benefits include lower input costs, improved liquidity, and enhanced predictability, enabling firms to scale, invest, and climb up the value chain. On the exports front, more competitive input costs, the ability to service low-value consignments, and a simpler tax environment can help India stake a stronger claim in global supply chains.

- However, success hinges on stringent implementation, strong enforcement of pass-through, state cooperation, and constant course correction. Realising the projected GDP gains and export growth will depend on the extent to which the reforms are translated into real savings for consumers and seamless operations for industry.

Recap: