Gold Monetisation Scheme: Economic Viability Amid Declining Global Capital Flows

Introduction:

A Gold Monetisation Scheme allows households, institutions (e.g. temple trusts, corporates), and banks to deposit idle/under-utilised gold (jewellery, coins, bars) with authorised institutions, earning interest, while the deposited gold is put to productive use (for lending to jewellers or industry). The aim is to mobilise the vast private stock of gold lying idle, reduce reliance on imports, improve domestic liquidity and channel domestic savings into development.

According to the World Investment Report 2025, global FDI flows fell by around 11 % in 2024, marking the second straight year of decline. Despite large cumulative gross FDI flows over the past two decades, more recently global volatility, rising cost of capital, and geopolitical risk have made external flows more unpredictable and fickle.

I. Supply-side & Resource Mobilisation Dimension

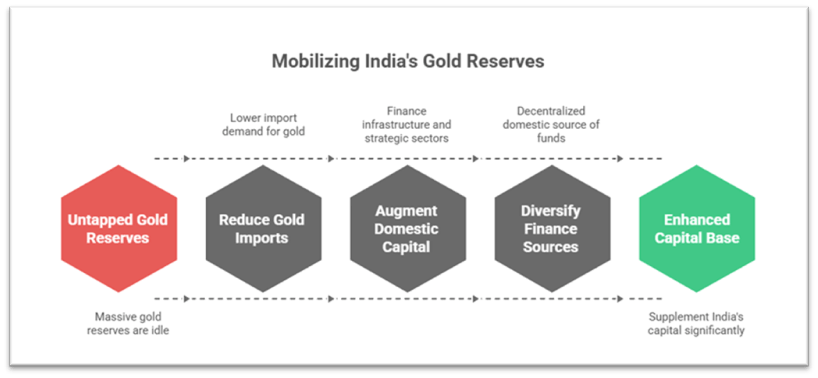

Massive Latent Stock

- Indian households cumulatively hold an estimated ~25,000 tonnes of gold, making it possibly the largest privately held gold reserve globally (worth trillions in USD value).

- This is a huge resource that, if partially mobilised, could supplement India’s capital base significantly.

Reduced Import Burden / Current Account Benefit

- India imports about 87 % of its gold demand, and gold imports contribute meaningfully to the trade deficit.

- Mobilising domestic gold could reduce the import demand, easing pressure on foreign exchange reserves and current account balance.

Augmenting Domestic Capital for Infrastructure / Development

- Even a modest mobilisation of 5–10 % of household gold could provide a large corpus for financing infrastructure, manufacturing or strategic sectors.

- Because the cost of interest on gold deposits could be lower than external borrowing, such mobilisation would reduce dependence on volatile external debt or foreign capital.

Diversification of Sources of Finance

- In an era when foreign capital is fickle, a trust-based gold scheme offers an alternative, decentralized, domestic source of funds.

- It helps in de-risking the economy from external capital shocks (capital flight, sudden stops).

Caveats / Risk Points

- Only a fraction of households may participate (liquidity preference, lack of trust, cultural attachment to keeping gold).

- The scheme must compete with other forms of savings or gold investments (Sovereign Gold Bonds, gold ETFs, etc.).

- Some of the gold may be low purity or hard to certify, increasing costs.

II. Cost, Interest Rate and Financial Viability Dimension

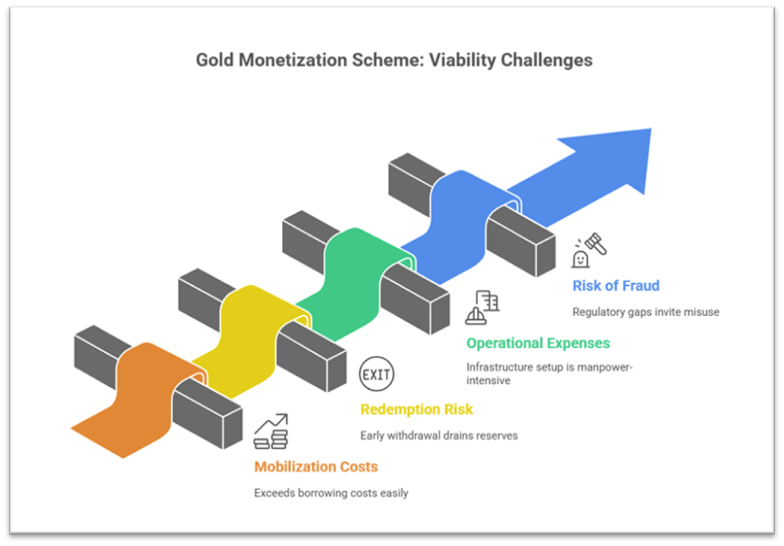

Cost of Mobilisation vs Borrowing Cost

- Interest to be paid to depositors must be moderate so that the scheme does not become an expensive burden. Projections suggest possible interest rates in the range 4.5 % to 6.5 % (if properly structured), which may be lower than cost of external borrowing or raising capital in volatile global markets.

- The scheme has to cover costs of assaying, refining, storage, logistics, security — these overheads can erode net viability.

Default, Liquidity and Redemption Risk

- Depositors might demand early withdrawal; provisions for premature redemption must be factored, and liquidity buffers kept (in INR rather than gold).

- Market volatility in gold prices can cause mismatch risk (if depositors redeem in INR equivalent when gold value swings).

Administrative and Operational Expenses

- Setting up and scaling a dense network of assaying & hallmarking centres, collection and purity verification infrastructure, secure logistics etc. is capital and manpower-intensive.

- Ongoing costs of quality assurance, insurance, warehousing, and auditing are nontrivial.

Risk of Arbitrage, Misuse or Fraud

- If regulatory or tax advantages are too generous, the scheme may get abused (e.g. gold laundering, shell entity deposits, over-statement of purity).

- Ensuring transparency, monitoring and control will require robust governance and technology safeguards.

Examples

- The original Gold Monetisation Scheme (GMS) launched in 2015 had some uptake, with mobilisations rising (in FY21, through gold schemes including GMS, sovereign bonds, etc, the government mobilised ~Rs 20,227 crore).

- However, in March 2025, the Indian government discontinued the medium-term and long-term gold deposit components, retaining only short-term deposit option, indicating constraints in cost or viability.

- Thus the scheme’s cost side is a crucial constraint and has already forced policy retrenchment.

III. Trust, Governance, Behavioural & Systemic Risks Dimension

Building Depositor Trust is Critical

- Households must believe that purity testing, valuation, security, redemption will work fairly and transparently.

- Any past scandals in hallmarking or fraud would deter participation unless the scheme is well insulated from trust deficits.

Frictions, Taxation, Regulatory Clarity

- Removal of GST, customs scrutiny, and other transactional friction is necessary to make the scheme attractive.

- If deposit interest or capital gains are taxed heavily, households may prefer to hold physical gold rather than deposit it.

Competition with Alternative Financial Vehicles

- Sovereign Gold Bonds (SGBs) already exist and give interest plus gold appreciation benefit; many investors prefer those for liquidity and safety.

- Gold ETFs, digital gold, and private sector gold savings offerings compete as substitutes.

Systemic and Financial Stability Risks

- Concentration risk: if large amount of gold is deposited with few banks, risk of default or mismanagement arises.

- If redemption commitments cannot be met (especially in periods of gold price volatility), it could strain banks’ balance sheets.

- Integration with the banking and capital markets needs to ensure that monetised gold does not become a source of fragility (e.g. running to convert to INR en masse).

Conclusion

- On balance, a trust-based Gold Monetisation Scheme is conditionally viable but not a panacea. Its success depends on strong institutional design, adequate scale, behavioural uptake, and risk controls.

- I largely agree with the argument that mobilising domestic gold is a strategic necessity in times of declining global capital flows, but I also believe that the economic challenges and risks are real and must be managed carefully.

- In the era of waning global capital flows, India cannot fully rely on external funding; unlocking domestic latent wealth, particularly gold, is both a pragmatic and strategic imperative. A trust-based gold monetisation scheme offers a promising route, but its viability is contingent on addressing cost structures, depositor trust, regulatory clarity, and systemic safeguards.

Recap: