Fiscal Discipline and Inflation Targeting in India: A Critical Analysis for Macroeconomic Stability

Fiscal discipline and inflation targeting form the core pillars of India’s macroeconomic stability framework. As inflation control becomes central to economic welfare, especially under the Flexible Inflation Targeting (FIT) regime, the interplay between these two policies determines how effectively India can manage growth, price stability, and long-term sustainability.

Introduction

• Macroeconomic stability in India increasingly hinges on the coordination between fiscal discipline and inflation targeting, particularly under the Flexible Inflation Targeting (FIT) framework, which mandates monetary policy to maintain inflation at 4 percent (+/–2 percent). Inflation control is vital because persistently high inflation acts as a regressive consumption tax, disproportionately burdening poorer households and eroding savings as well as investment decisions.

• India’s experience since the adoption of FIT in 2016, following earlier reforms such as the phasing out of automatic monetisation (1994) and the FRBM Act (2003), shows that both frameworks must function in tandem to maintain credibility, anchor inflation expectations, and support stable growth.

• The evolving domestic environment, marked by global commodity price volatility, fiscal stress, and supply-side shocks, makes it essential to critically assess the interplay between fiscal and monetary frameworks as India’s FIT review approaches March 2026.

1. Inflation Targeting and Its Effectiveness in the Indian Context

a) Headline vs Core Inflation: Choosing the Right Nominal Anchor

• Headline inflation better reflects consumer welfare, especially for low-income households whose consumption baskets are dominated by food and fuel. Episodes such as the 2019–2023 food and fuel price spikes illustrate how supply shocks can transmit into wages and core inflation when aggregate demand remains accommodative.

• Core inflation alone cannot inform monetary policy adequately because food inflation often triggers second-round effects, including upward wage revisions in MNREGA-linked rural markets and increased pricing decisions in MSMEs. This blurs the distinction between relative price movements and general inflation.

• Case studies from Brazil and South Africa show that inflation targeting frameworks that focus solely on core inflation failed to capture food-related inflation persistence, leading to delayed policy responses.

b) Acceptable Level of Inflation and Growth Trade-offs

• The longstanding debate around the Phillips Curve shows only a short-run trade-off between growth and inflation. A non-linear relationship between India’s post-1991 growth and inflation patterns indicates that inflation above roughly 4 percent correlates with slower growth, validating the current target.

• Threshold inflation analyses for emerging markets show that inflation above 6–7 percent threatens investment certainty, while moderate inflation supports resource allocation and expectations stability.

• Successful episodes like India’s post-2016 period, despite global shocks (COVID-19, Ukraine conflict), demonstrate how well-anchored expectations under FIT prevented inflation from becoming entrenched even when temporary breaches occurred.

c) Requirements for an Effective Inflation Targeting Framework

• Inflation targeting demands institutional credibility, including independence for the Monetary Policy Committee (MPC), regular publication of forecasts, and transparent communication.

• The success of FIT also requires supply-side policy alignment, which India attempted through measures such as buffer stock management, import duty adjustments, and Minimum Export Price (MEP) interventions in essential commodities.

• Examples such as New Zealand and the UK highlight that inflation targeting is effective when fiscal policy avoids excessive deficits, preventing monetary policy from compensating for fiscal slippages.

2. Fiscal Discipline as a Complement to Inflation Targeting

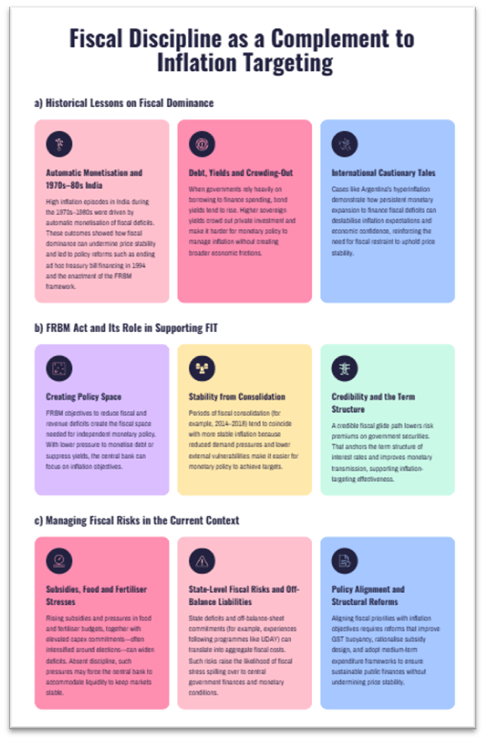

a) Historical Lessons on Fiscal Dominance

• India’s high inflation episodes during the 1970s–1980s, driven by automatic monetisation of fiscal deficits, highlight how fiscal dominance undermines price stability. This prompted reforms, including discontinuation of ad hoc treasury bills in 1994 and the FRBM Act.

• When governments rely heavily on borrowing for expenditure, bond yields rise, crowding out private investment and complicating inflation management.

• International examples such as Argentina’s hyperinflation underscore how monetary expansion to finance deficits destabilizes inflation expectations.

b) FRBM Act and Its Role in Supporting FIT

• The FRBM’s goals of reducing fiscal deficit and eliminating revenue deficit create space for monetary policy to act without pressure to monetise debt or suppress yields.

• When fiscal consolidation progresses, as seen in 2014–2018, inflation remains more stable due to reduced demand pressures and lower external vulnerability.

• The fiscal glide path’s credibility influences risk premiums on government securities, which in turn anchor the term structure of interest rates, aiding monetary transmission.

c) Managing Fiscal Risks in the Current Context

• Rising subsidies, food and fertilizer stresses, and increased capex commitments risk widening deficits, especially during elections. Without discipline, these pressures could shift the burden onto RBI to maintain liquidity.

• State government deficits add to aggregate fiscal stress, as seen in instances of Ujjwal DISCOM Assurance Yojana (UDAY) where off-balance-sheet liabilities eventually translated into fiscal costs.

• The need to align fiscal priorities with inflation objectives requires reforms in GST buoyancy improvement, rationalised subsidies, and medium-term expenditure frameworks.

3. Interplay Between Fiscal and Monetary Policy for Macroeconomic Stability

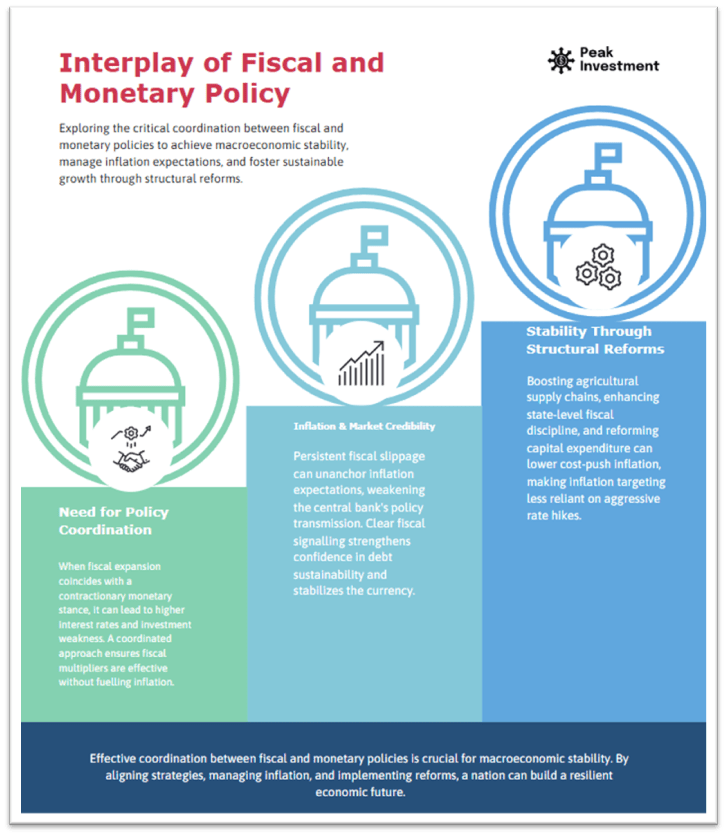

a) Need for Policy Coordination to Prevent Conflicting Signals

• When fiscal expansion coincides with a contractionary monetary stance, the results can include higher interest rates, weaker investment, and exchange rate volatility. For example, excessive open market borrowing in 2020–2022 forced RBI to engage in liquidity operations that complicated inflation control.

• A coordinated approach ensures that fiscal multipliers remain effective without fuelling inflation, especially when public investment targets supply bottlenecks.

• Global experiences during COVID-19 (e.g., EU coordinated fiscal-monetary response) highlight the importance of complementarities.

b) Impact on Inflation Expectations and Market Credibility

• Persistent fiscal slippage can unanchor inflation expectations, prompting higher term premiums on government bonds. This weakens RBI’s ability to transmit policy rates to lending markets.

• Clear fiscal signalling strengthens confidence in debt sustainability and stabilizes the rupee, which matters for imported inflation.

• Successful coordination examples include India’s consolidation period (2003–2008) where fiscal prudence reinforced monetary tightening to bring inflation down.

c) Ensuring Stability Through Structural Reforms

• Boosting agricultural supply chains through schemes like PMKSY, e-NAM, and Operation Greens reduces food inflation volatility, reducing the burden on monetary tightening.

• Enhancing state-level fiscal discipline through IFMIS, outcome budgeting, and revised borrowing limits helps lower systemic inflation pressures.

• Reforms targeting capital expenditure, logistics, electricity pricing, and rural market linkages can lower cost-push inflation, making inflation targeting less reliant on aggressive rate hikes.

Conclusion:

• Fiscal discipline and inflation targeting are mutually reinforcing pillars of India’s macroeconomic stability. While FIT helps anchor expectations and maintain price stability, fiscal prudence ensures that monetary policy operates without being constrained by debt obligations or liquidity pressures.

• Going forward, India needs a credible fiscal consolidation path, stronger institutional mechanisms under FRBM, and a refined inflation-targeting framework that reflects long-run growth prospects.

• With India aiming for sustained high growth through the decade, maintaining inflation near 4 percent while ensuring fiscal sustainability will be essential to protect the poor, enhance investment confidence, and safeguard macroeconomic resilience.

Recap: