Tax Buoyancy and Fiscal Discipline: Why Indirect Tax Buoyancy Remains Weak Under GST

Tax buoyancy plays a critical role in maintaining fiscal discipline by ensuring that government revenues grow in tandem with economic expansion. In India, while direct taxes have shown strong responsiveness to GDP growth, the persistently low indirect tax buoyancy—despite the maturation of the GST regime—has emerged as a key challenge for sustainable fiscal consolidation.

Introduction:

- Tax buoyancy refers to the responsiveness of tax revenues to changes in national income, indicating how efficiently a tax system translates economic growth into fiscal resources.

- An economy-wide buoyancy close to or above 1 implies that revenues grow at least proportionately with GDP, strengthening fiscal discipline, reducing dependence on borrowing, and enabling sustainable public expenditure.

- In India’s recent fiscal trajectory, while overall tax projections have been realistic, the divergence between direct tax buoyancy above unity and indirect tax buoyancy significantly below unity has raised concerns.

Body:

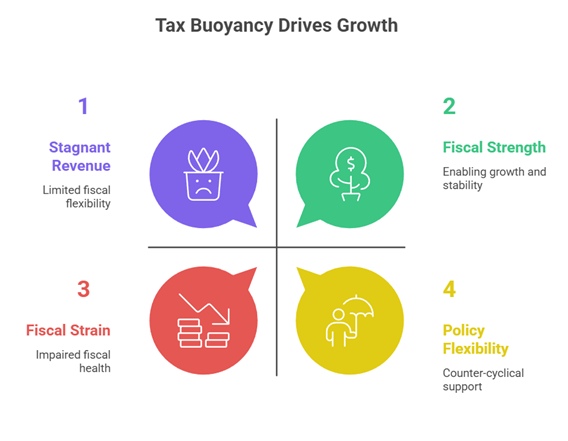

I. Significance of Tax Buoyancy for Fiscal Discipline

1. Enabling Sustainable Public Finances

- A high tax buoyancy ensures that revenue growth organically keeps pace with economic expansion, reducing reliance on deficit financing and stabilising the debt–GDP ratio over time.

- When buoyancy remains strong, governments can maintain capital expenditure-led growth without crowding out private investment.

- Example: Post-pandemic fiscal consolidation was facilitated by steady direct tax buoyancy supporting expenditure commitments.

2. Supporting Counter-cyclical Fiscal Policy

- Buoyant taxes provide governments the flexibility to expand spending during downturns without permanently impairing fiscal health.

- Automatic stabilisers function effectively only when tax systems are elastic to income changes.

- Case Study: Pandemic-era welfare spending was sustained partly due to revenue resilience from income-linked taxes.

3. Improving Expenditure Quality and Credibility

- Predictable revenue flows from buoyant taxes allow better medium-term expenditure planning.

- Strong buoyancy enhances the credibility of fiscal rules and investor confidence.

- Government Initiative: Medium-term fiscal frameworks rely on stable buoyancy assumptions.

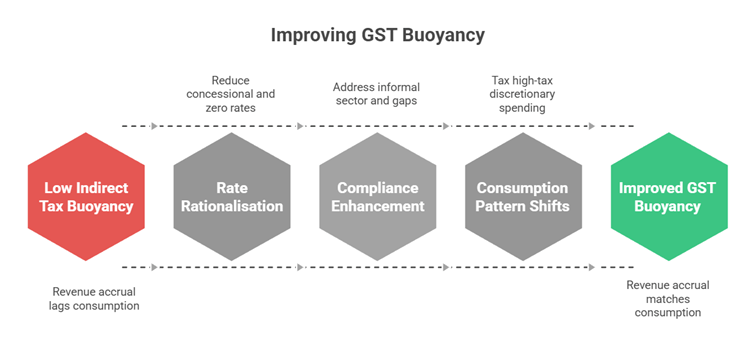

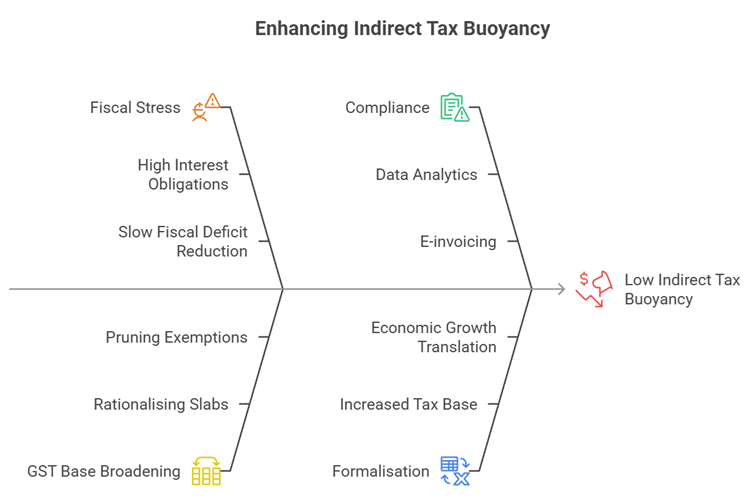

II. Reasons for Persistently Low Indirect Tax Buoyancy

1. Structural Constraints within the GST Framework

- Despite its maturity, GST continues to face rate rationalisation delays.

- Frequent exemptions and inverted duty structures dilute the tax base.

- Example: Multiple GST slabs reduce overall revenue elasticity.

2. Compliance and Administrative Challenges

- Informal sector dominance and compliance gaps limit effective tax capture.

- Input tax credit complexities create incentives for under-reporting.

- Case Study: MSMEs often remain below threshold limits, muting buoyancy.

3. Macroeconomic and Consumption Pattern Shifts

- Consumption growth has shifted toward essential and low-tax items.

- Services and digital consumption remain under-taxed.

- Example: Post-inflation household spending prioritising necessities dampens GST growth.

III. Implications and Reform Pathways to Enhance Indirect Tax Buoyancy

1. Fiscal Stress and Consolidation Trade-offs

- Low indirect tax buoyancy increases borrowing pressures.

- High interest payments reduce fiscal space for development.

- Example: Rising interest–revenue ratios amplify fiscal stress.

2. Need for GST Base Broadening and Rate Rationalisation

- Pruning exemptions and rationalising slabs can realign revenues with consumption.

- Simplification improves compliance and efficiency.

- Government Initiative: GST Council reform agenda targets structural distortions.

3. Strengthening Compliance through Technology and Formalisation

- Data analytics, e-invoicing, and inter-agency coordination reduce evasion.

- Formalisation expands the effective tax base.

- Case Study: Invoice-matching systems have improved large-firm compliance.

Conclusion:

- Tax buoyancy is central to durable fiscal discipline and macroeconomic stability.

- Weak indirect tax buoyancy reflects structural and demand-side challenges within GST.

- Rate rationalisation, base broadening, and technology-driven compliance can restore buoyancy and ease fiscal pressures.

Recap: