Currency Devaluation in India: Why It Fails When Inflation Is Low and Trade Barriers Are Non-Economic

Currency devaluation in India refers to a deliberate or market-driven decline in the value of a country’s currency against foreign currencies, often expected to boost exports and correct external imbalances. In India’s current economic scenario, however, this traditional adjustment mechanism is losing relevance.

Despite a robust growth trajectory, subdued inflation well below the central bank’s tolerance band, and a manageable current account deficit, the rupee has witnessed a sharp depreciation driven largely by capital outflows and geopolitical trade frictions rather than macroeconomic weaknesses.

This context underscores why devaluation becomes an ineffective and even counterproductive remedy when inflation is low and trade barriers arise from non-economic considerations.

I. Weak Export-Stimulus Channel under Low Inflation and Global Value Chains

Diminished competitiveness gains due to rising import intensity of exports

India’s manufacturing and services exports are increasingly embedded in global value chains, with high dependence on imported intermediates such as electronic components, chemicals, and energy inputs. As a result, any rupee depreciation raises input costs, neutralising the price advantage that devaluation traditionally offers exporters.

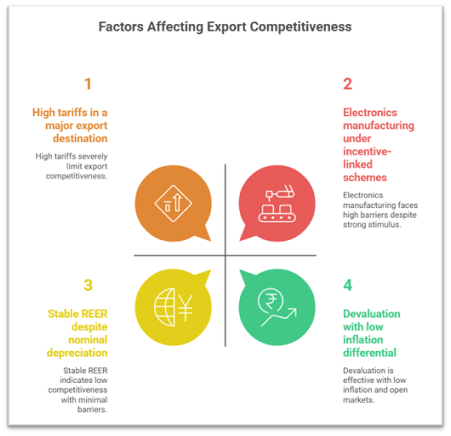

Case Study: Electronics manufacturing — assembly-led export growth under incentive-linked schemes faces higher imported component costs when the rupee weakens, compressing margins rather than expanding export volumes.

Absence of inflation differential undermines the rationale for devaluation

Devaluation is most effective when domestic inflation exceeds that of trading partners, necessitating a correction through the Real Effective Exchange Rate (REER). With India’s inflation lower than that of several advanced economies, the rupee is not fundamentally overvalued, making depreciation economically unjustified.

Example: Stable REER despite nominal depreciation — inflation-adjusted competitiveness remains broadly aligned, limiting export responsiveness.

Limited demand response under restrictive trade environments

Even if price competitiveness improves marginally, exports cannot expand meaningfully when key markets impose prohibitive tariffs or regulatory barriers unrelated to cost efficiency.

Case Study: High tariffs in a major export destination — steep import duties negate any currency-led price advantage, rendering devaluation ineffective as a trade strategy.

II. Inflationary and External Sector Risks from Currency Depreciation

Imported inflation through essential commodities

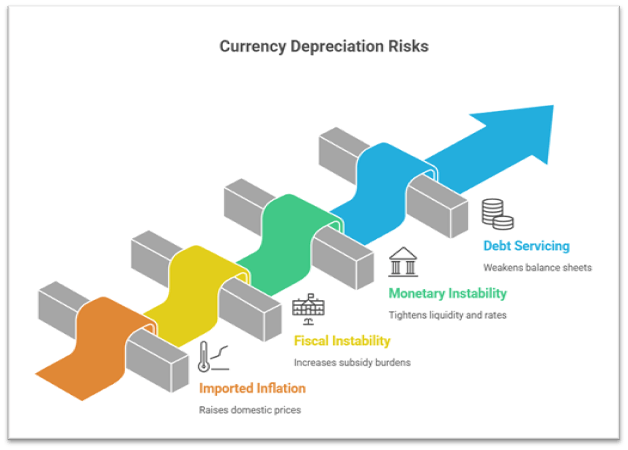

India’s import basket is dominated by inelastic essentials, with crude oil, fertilisers, and edible oils forming a substantial share. A weaker rupee directly raises domestic prices, risking a reversal of hard-won price stability.

Real-Life Example: Energy pass-through — higher landed crude costs transmit into transport, logistics, and food prices, amplifying economy-wide inflationary pressures.

Adverse impact on fiscal and monetary stability

Rising import costs increase subsidy burdens and complicate fiscal consolidation, while the central bank may be forced to tighten liquidity or interest rates to anchor inflation expectations.

Example: Fuel and fertiliser support mechanisms — depreciation raises subsidy requirements, constraining developmental spending.

Debt servicing and balance sheet stress

External commercial borrowings and foreign currency liabilities become costlier in rupee terms, weakening corporate and sovereign balance sheets.

Case Study: Infrastructure and power sectors — projects with foreign-denominated loans face higher repayment obligations, affecting financial viability.

III. Capital Flows, Geopolitics and the Limits of Exchange Rate Adjustment

Capital outflows driven by geopolitical uncertainty, not fundamentals

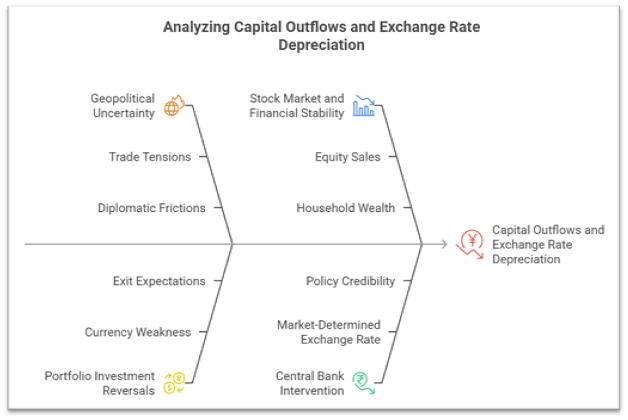

Recent rupee depreciation has been accompanied by net capital outflows, reflecting investor concerns over trade tensions and diplomatic frictions rather than macroeconomic instability. Devaluation cannot address such sentiment-driven exits.

Example: Portfolio investment reversals — currency weakness reinforces exit expectations, creating a self-reinforcing cycle of depreciation and outflows.

Stock market and financial stability spillovers

Capital outflows through equity sales directly depress stock indices and household wealth, affecting consumption and investment confidence.

Case Study: Foreign portfolio sell-offs — currency depreciation coinciding with equity exits magnifies volatility in domestic financial markets.

Role of central bank intervention and credibility

Under a market-determined exchange rate regime, monetary authorities intervene not to defend a specific level but to smooth volatility and prevent disorderly movements. Excessive reliance on depreciation risks eroding policy credibility without resolving the underlying non-economic pressures.

Example: Asymmetric foreign exchange intervention — moderating abrupt falls to maintain orderly market conditions while preserving long-term stability.

Conclusion:

India’s current experience demonstrates that currency devaluation in India is an ineffective remedy when inflation is low and trade barriers are geopolitical rather than economic. With inflation well-anchored, a manageable external balance, and depreciation driven by capital flows responding to diplomatic tensions, weakening the currency offers limited export gains while heightening inflationary, fiscal, and financial risks.

A more durable path lies in diplomatic engagement to resolve trade frictions, policy predictability to restore investor confidence, and measured central bank intervention to smooth volatility.

Strengthening domestic value addition, diversifying export markets, and sustaining macroeconomic credibility can stabilise the currency more effectively than relying on devaluation, ensuring growth remains resilient without compromising price and financial stability.

Recap: