India’s Strategy to Diversify Energy Imports Explained

Energy security is increasingly intertwined with national security, foreign policy, and economic stability. India’s strategy to diversify energy imports is critical as the country imports over 85% of its crude oil and more than 50% of its natural gas (Ministry of Petroleum & Natural Gas, 2025), making it highly vulnerable to global disruptions. In FY 2023–24, oil and gas alone accounted for $170 billion, nearly 25% of India’s $677 billion merchandise import bill (DGFT data).

Events like the 1973 Oil Embargo, the 2022 Russia-Ukraine war, and the June 2025 Israel-Iran flashpoint underline how geopolitical tensions can choke supply chains. Against this backdrop, India’s diversification strategy—ranging from sourcing Russian discounted crude to exploring African and Latin American suppliers—forms the backbone of its energy sovereignty doctrine.

Strategic Merits of Diversification

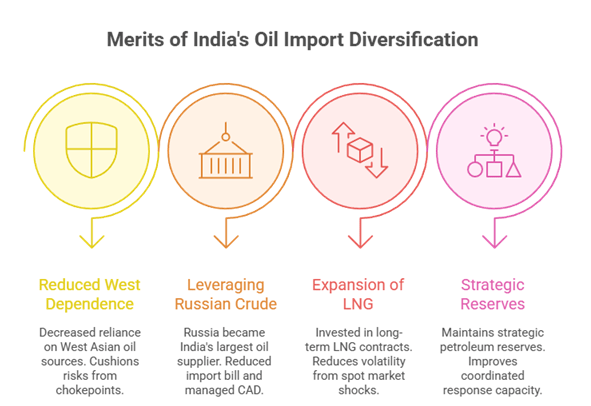

Reduced West Asian Dependence

- Historically, India sourced 60% of crude from West Asia, but by 2024–25 this fell below 45% (S&P Global Commodities at Sea).

- Diversification into Russia, Africa (Nigeria, Angola), and Latin America (Brazil, Mexico) cushions risks from Strait of Hormuz chokepoints.

- Example: During the June 2025 Israel–Iran tension, India’s higher share of Russian oil provided stability even as Brent prices threatened to spike above $103/barrel.

Leveraging Russian Discounted Crude

- Since 2022, Russia has become India’s single largest oil supplier (35–40% of imports) from just 2% before the Ukraine war.

- The discounted crude helped India reduce its import bill and manage CAD, while allowing refiners like IOC and Reliance to profit through re-exports.

- Case Study: India emerged as Europe’s top refined products supplier in 2023, showing economic gains from arbitrage opportunities.

Expansion of LNG Partnerships

- India has invested in long-term LNG contracts with Qatar (Qatargas extension till 2048), Russia’s Arctic LNG-2, and Mozambique LNG.

- This reduces volatility from spot market shocks as seen during the 2021–22 LNG price surge in Europe.

- Government initiative: India’s National Gas Grid expansion (33,500 km target by 2030) integrates diversified LNG into the domestic economy.

Institutional Mechanisms and Strategic Reserves

- India maintains 5.3 MMT Strategic Petroleum Reserves in Visakhapatnam, Mangalore, and Padur, with expansion planned.

- Frameworks like International Energy Agency (IEA) association since 2017 improve coordinated response capacity.

- Example: During COVID-19 2020 crude price collapse, India filled reserves at low cost, demonstrating foresight in storage planning.

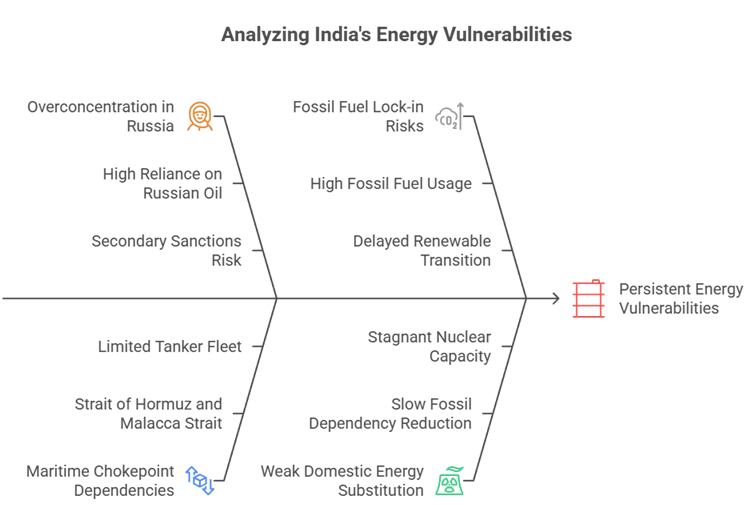

Persistent Vulnerabilities in India’s Approach

Overconcentration in Russia Post-2022

- While reducing West Asia dependence, 35–40% reliance on Russian oil exposes India to secondary sanctions risk from the US/EU.

- Example: Indian banks faced delays in processing payments in 2023–24 due to sanctions compliance uncertainty.

- This makes diversification look like substitution rather than true risk spreading.

Maritime Chokepoint Dependencies

- Nearly 70% of India’s crude flows through the Strait of Hormuz and Malacca Strait, both geopolitically sensitive zones.

- Case Study: Houthi attacks on Red Sea shipping in 2024 forced Indian refiners to reroute cargos at higher insurance and freight costs.

- Limited domestic tanker fleet (SCI fleet size ~70 ships) increases vulnerability to global freight disruptions.

Fossil Fuel Lock-in Risks

- Despite diversification, fossil fuels still meet over 80% of India’s energy demand (BP Statistical Review 2024).

- Heavy investment in oil diplomacy may delay transition into renewables, risking carbon lock-in at a time of global net-zero race.

- Example: Spain-Portugal 2025 blackout shows over-reliance on intermittent renewables is risky, but India still lacks a balanced baseload transition plan.

Weak Domestic Energy Substitution

- Despite programs like E20 ethanol blending and SATAT CBG scheme, fossil dependency reduction is slow.

- India’s nuclear capacity remains stagnant at 8.8 GW, contributing barely 2% of electricity generation.

- Example: Japan post-Fukushima (2011) initially abandoned nuclear, later revived it—India’s delays show hesitation in bold choices.

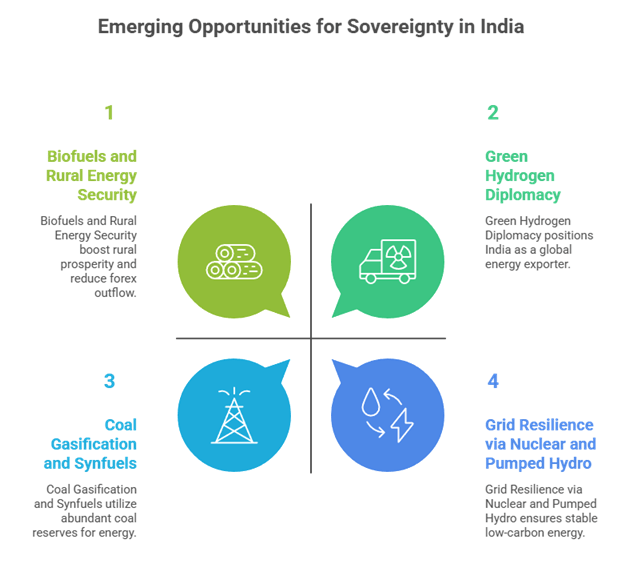

Emerging Opportunities for Sovereignty

Coal Gasification and Synfuels

- With 150+ billion tonnes of coal reserves, India can use gasification and carbon capture for syngas, methanol, and fertilizers.

- Case Study: China’s coal-to-chemicals industry has scaled syngas and methanol, offering a model for India.

- Policy: National Coal Gasification Mission (2021) targets 100 MTPA gasification by 2030.

Biofuels and Rural Energy Security

- The ethanol blending programme transferred ₹92,000 crore to farmers, reducing forex outflow.

- Compressed Biogas (CBG) under SATAT improves soil organic carbon (from current 0.5% to target 2.5%).

- Case Study: Brazil’s Proálcool ethanol programme demonstrates how biofuels can simultaneously ensure rural prosperity and energy security.

Green Hydrogen Diplomacy

- India’s National Green Hydrogen Mission (2023) targets 5 MMT/year by 2030, focusing on electrolyser manufacturing and storage.

- Example: EU–India Hydrogen Partnership (2023) aims to build a global supply chain independent of Middle Eastern hydrocarbons.

- This not only diversifies imports but positions India as an exporter of energy solutions.

Grid Resilience via Nuclear and Pumped Hydro

- Nuclear small modular reactors (SMRs) and thorium-based research can provide dispatchable low-carbon baseload.

- Pumped hydro (175+ potential sites identified by CEA) can balance solar/wind intermittency.

- Case Study: China’s 30 GW pumped hydro capacity demonstrates large-scale feasibility that India can emulate.

Conclusion

India’s diversification strategy has undeniably reduced exposure to singular risks such as West Asian supply shocks. By shifting crude sourcing from 60% West Asia to 45%, leveraging Russian discounts, and expanding LNG deals, it has strengthened short-term resilience. Yet, the overdependence on Russia, persistent chokepoint vulnerabilities, and slow domestic transition expose India to medium-term risks.

The way forward lies in embracing energy realism—treating sovereignty not as a function of cheaper barrels but as the ability to secure uninterrupted, affordable, and indigenous energy. As IEA’s World Energy Outlook 2024 warns of structurally tight fossil supply, India must anchor its five-pillared doctrine—coal gasification, biofuels, nuclear, green hydrogen, and pumped hydro—to avoid being hostage to external shocks.

Recap: