Lower Oil Prices: A Short-Term Reprieve for India's Economy, but a Warning on Energy Dependence

The global oil market remains central to the economic and strategic calculus of major energy-importing nations, and for India the stakes are unusually high. The **decline in global oil prices** offers India a short-term economic reprieve but also underscores the cyclical vulnerability of its energy dependence. As of the most recent data, India’s crude oil import dependency stands at around 88 per cent for the fiscal year ending March 2025.

Global supply is now rising faster than demand, with the International Energy Agency (IEA) forecasting a possible surplus of up to 4 million barrels per day in 2026. The statement that “the **decline in global oil prices** offers India a short-term economic reprieve but also underscores the cyclical vulnerability of its energy dependence” thus captures both the immediate upside and the underlying structural risk.

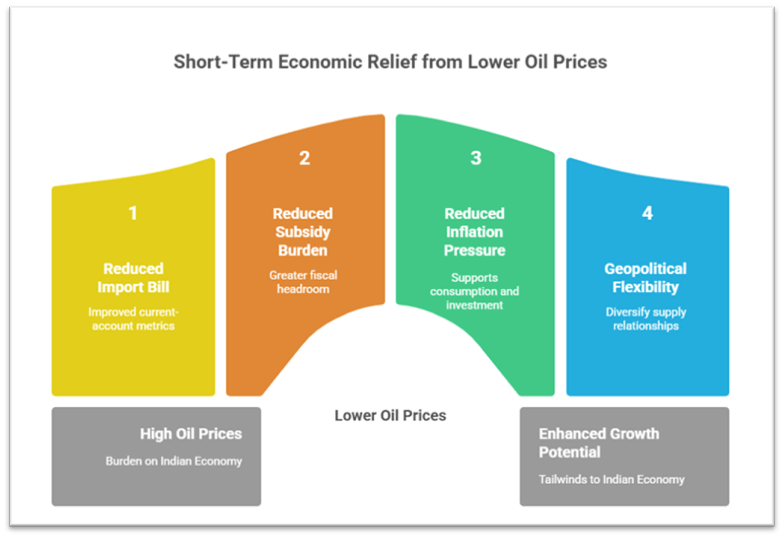

I. Short-Term Economic Relief from Lower Oil Prices

A. Improved Imports and Current Account

- With global oil prices under pressure (e.g., Brent forecast to average around US $62/b in Q4 2025 and possibly US $52/b in 2026). Lower prices reduce the value of India’s oil import bill; for instance, India imports more than 230 million metric-tonnes (MMT) of crude in FY 2023-24 (approximately) with an import bill running well over US $130 billion. That translates into improved current-account metrics.

- The fiscal burden of subsidies on transport fuel, petrol/diesel for consumers, and fertiliser whose feedstock is crude, is eased when crude prices fall—giving greater fiscal headroom for government capital expenditure.

- Lower oil prices also exert downward pressure on domestic inflation via reduced fuel input cost and transport cost, thereby indirectly supporting consumption and investment.

B. Reduced Subsidy and Inflation Pressure

- When crude and refined product prices ease, the government’s subsidy burden (either via direct price support or via under-recoveries of state-owned refiners) is lower; this helps maintain fiscal discipline and supports credit-offtake in key sectors like infrastructure.

- Lower fuel and transport cost feed into lower headline inflation, which gives the central bank greater flexibility in monetary policy and supports private investment and consumer spending.

- The combination of lower import bill and lower inflation can enhance India’s growth potential in the near-term, giving what can be described as a “tailwind” to an economy still growing robustly (India GDP growth around 7-8 % in recent years).

C. Geopolitical & Strategic Option Space

- A lower oil‐price environment grants India greater flexibility in sourcing, including from discounted barrels (for example, from Russia) without excessive cost burden. For instance, Russia’s share of India’s crude imports rose to ~35-40 % in 2024.

- With less pressure on oil import costs, India can diversify supply relationships (for example integrating more Middle East/UAE/Iraq supply) and build strategic petroleum reserves.

- A pragmatic lower‐price window gives India time and space to implement structural reforms in energy and accelerate transition without emergency cost pressures.

II. Structural Vulnerabilities & Cyclical Risks

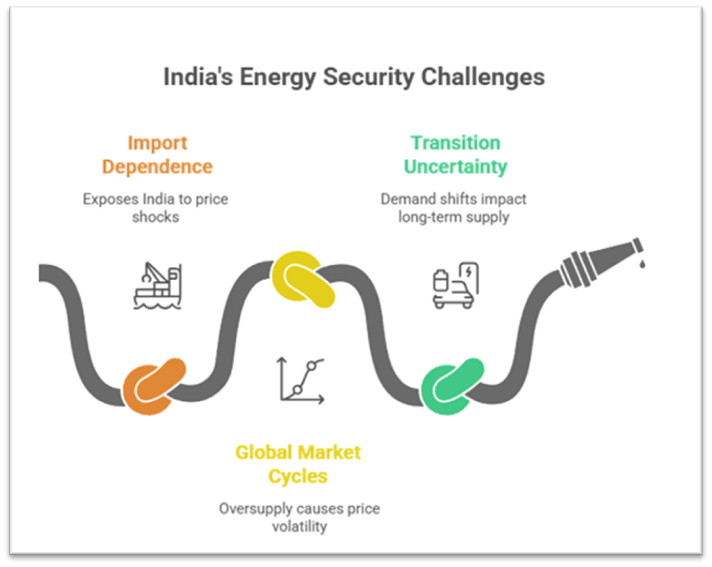

A. Heavy Import Dependence and External Vulnerability

- India’s crude oil import dependence has reached approximately 89 % of consumption in 2023–24. This exposes India to external price shocks, supply disruptions, freight risk, geopolitical risk, and currency‐risk through its dollar‐denominated oil import bill.

- India already accounts for perhaps 25 % of the growth in global oil consumption over 2024-25. As oil import volumes rise, even at stable or lower price levels, the total bill could increase, raising vulnerability.

- The concentration of supplies (Russia + Middle East ~ 80 % of Indian crude imports) means supply disruptions (e.g., sanctions, regional conflict) have outsized effect.

B. Global Market Cycles, Oversupply & Price‐Volatility

- The global market is subject to structural gluts: supply from non-OPEC+ (US shale, Brazil, Guyana) is rising, while demand growth is being revised downward. The IEA projects only ~0.7 mbd demand growth in 2025 even as supply may grow ~1.6 mbd.

- A prolonged oversupply means downward pressure on prices, but the oil market is cyclical—sharp rebounds are possible if supply is disrupted, or demand recovers. This implies India’s benefit from low prices may be short‐lived.

- The divergence in outlooks between major players (IEA sees surplus, OPEC sees near-balance) introduces strategic ambiguity and risk of policy missteps or sudden price shocks.

C. Transition & Demand Uncertainty

- On the demand side, mature markets (OECD) are flat or declining; the rise of EVs and climate policy mean oil demand growth is slowing. Global oil demand may peak by 2027-30 in some scenarios.

- India’s own growth trajectory means rising energy demand; but if global prices stay low or decline in real terms, the lethargy in investment in conventional upstream may reduce security of supply in the longer run.

- The temptation to rely solely on low-price relief may undermine urgency of structural reforms (e.g., energy efficiency, renewables, diversification) thereby cementing vulnerability.

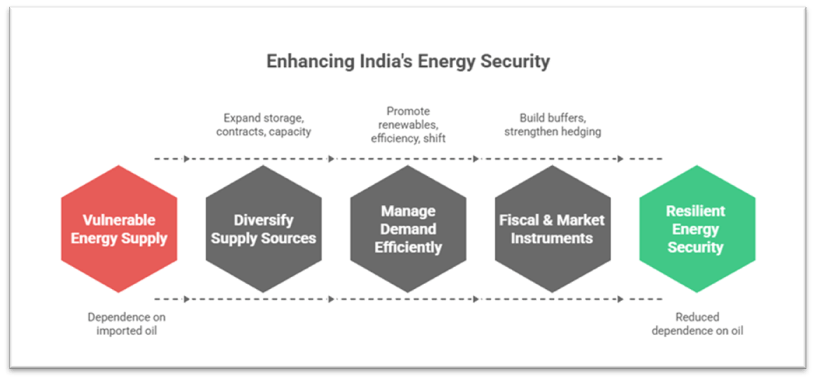

III. Policy & Strategic Imperatives for India

A. Diversify Supply & Build Strategic Resilience

- Expand storage capacity: India’s strategic petroleum reserve programme (e.g., Cavern storage at Mangalore, Vishakapatnam) needs acceleration to buffer supply shocks.

- Diversify geography of supply (Latin America, Africa, Central Asia) and expand long-term contracts rather than spot purchases (thus curbing exposure to spot price spikes).

- Enhance domestic upstream & refining capacity: For example, ramp up exploration & production through fields in Rajasthan, offshore, and strengthen refining capacity to reduce dependence on imported finished products.

B. Manage Demand via Efficiency & Transition

- Promote energy efficiency in transport (FAME II, GatiShakti National Master Plan), mandate fuel economy norms, encourage shift to EVs and public transport.

- Ramp up renewables (Solar Rooftop, Wind, Green Hydrogen Mission) to reduce growth in oil consumption—oil’s share in primary energy supply can thus decline.

- Encourage modal shift (rail freight over road, electric buses) and integrate petrochemical feedstock strategy so that oil demand growth is less steep.

C. Fiscal & Market Instruments

- Use lower oil prices to build fiscal buffers (reduce subsidies, strengthen sovereign wealth/sovereign oil funds) which can be deployed when prices surge.

- Strengthen the hedging and derivative instruments for oil procurement, and enhance transparency in pricing and imports.

- Encourage domestic refining of heavier / discounted crudes (e.g., from Russia) to capture margins, reduce import bill; integrate with trade diplomacy (e.g., India-Russia oil deals) consistent with multilateral obligations.

Conclusion:

The current **decline in global oil prices** offers India meaningful short-term relief—improving its import bill, reducing inflation and subsidies, and enhancing strategic space. However, this relief must not engender complacency.

India’s high import dependency (~88 %) and the cyclicality of the oil market mean that today’s benefit could become tomorrow’s vulnerability if supply shocks, demand resurgence or geopolitical disruptions occur. To turn the temporary reprieve into durable advantage, India must use this window to deepen supply diversification, accelerate demand‐side reforms (efficiency, transition) and build fiscal and strategic buffers.

With global growth projected at ~3.0 % for 2025 and 2026, per the IMF forecast, and oil supply outpacing demand, the margin for error is narrow. If India successfully embeds these reforms, it will emerge not just as a beneficiary of lower oil prices but as a more resilient economy less buffeted by global oil cycles.

RECAP: