Nominal GDP Revision India: Impact on Fiscal Ratios and Policy Planning

Nominal GDP Revision India has emerged as a critical macroeconomic development with the introduction of the new GDP series (base year 2022–23), leading to a downward revision of GDP estimates by around 3–4%. This recalibration has important implications for fiscal ratios, macroeconomic indicators, and policy planning.

Introduction

- Gross Domestic Product (GDP) represents the aggregate monetary value of all final goods and services produced within an economy over a specified period, and serves as the principal metric for assessing macroeconomic performance.

- With the introduction of a new GDP series (base year 2022–23), India’s nominal GDP estimates for recent years have been revised downward by around 3–4%, even as structural sectoral shares remain broadly stable (Primary ~21%, Secondary ~26%, Tertiary ~53%).

- This recalibration, based on improved methodologies such as double deflation, expanded corporate coverage (MCA, LLPs), and integration of HCES, ASUSE and PLFS datasets, has significant implications for fiscal ratios and macroeconomic policy calibration.

1. Implications for Fiscal Ratios and Macroeconomic Indicators

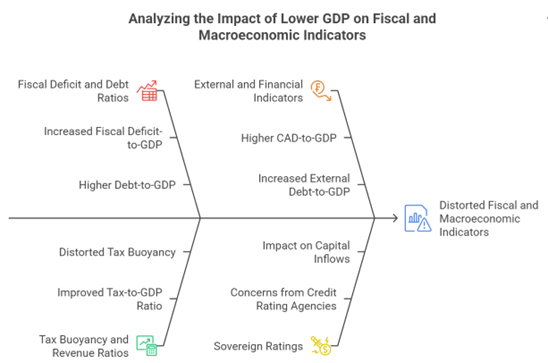

1.1 Impact on Fiscal Deficit and Debt Ratios

- A lower nominal GDP denominator mechanically raises key fiscal ratios such as Fiscal Deficit-to-GDP and Debt-to-GDP, even if absolute borrowing remains unchanged, thereby affecting perceived fiscal prudence.

- For instance, if fiscal deficit remains constant but GDP shrinks by 3–4%, the ratio may rise beyond targets under the Fiscal Responsibility and Budget Management (FRBM) framework, complicating fiscal consolidation commitments.

- Example – India’s Medium-Term Fiscal Policy: Targets such as reducing fiscal deficit below 4.5% of GDP by 2025–26 may appear more challenging under revised GDP estimates.

1.2 Alteration in Tax Buoyancy and Revenue Ratios

- Tax-to-GDP ratio improves arithmetically due to lower GDP, potentially overstating revenue performance without real improvement in tax collection efficiency.

- This may distort analysis of tax buoyancy, which is critical for assessing responsiveness of tax revenues to economic growth.

- Case Study – GST Performance: Rising GST collections may appear stronger relative to GDP, even if driven by inflation or compliance improvements rather than real economic expansion.

1.3 Effects on External and Financial Indicators

- Ratios such as Current Account Deficit (CAD)-to-GDP, External Debt-to-GDP, and Investment-to-GDP are similarly affected, influencing global investor perception and sovereign ratings.

- A higher debt ratio could raise concerns among credit rating agencies, despite no real deterioration in macro fundamentals.

- Example – Sovereign Ratings Sensitivity: Agencies often benchmark India against emerging economies using GDP-relative indicators, making revisions significant for capital inflows.

2. Implications for Policy Planning and Governance

2.1 Recalibration of Fiscal Policy and Expenditure Planning

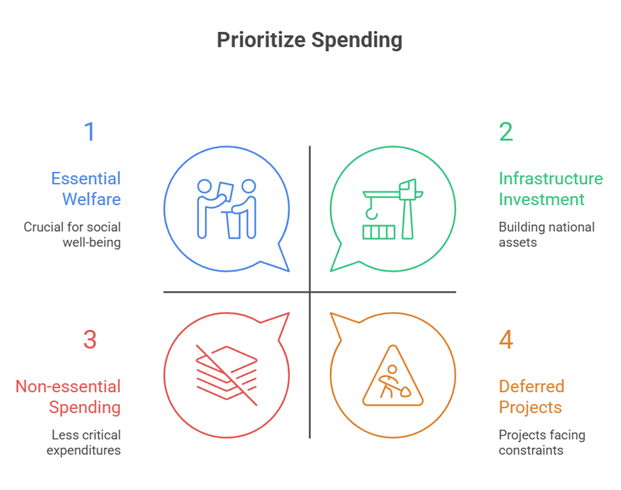

- Government expenditure priorities may require reassessment as fiscal space appears tighter due to elevated deficit ratios.

- This could lead to reprioritisation between capital expenditure (infrastructure, logistics) and revenue expenditure (subsidies, welfare).

- Example – National Infrastructure Pipeline (NIP): Financing large-scale infrastructure may face tighter fiscal constraints, necessitating innovative financing like PPP models.

2.2 Implications for Centre-State Fiscal Relations

- Gross State Domestic Product (GSDP) estimates depend on national aggregates; inaccuracies or downward revisions complicate tax devolution and Finance Commission transfers.

- Allocation formulas based on income distance and fiscal capacity may be distorted, impacting poorer states disproportionately.

- Case Study – GST Compensation Mechanism: States’ revenue expectations linked to growth projections may face recalibration under revised GDP base.

2.3 Impact on Welfare and Development Metrics

- Several development indicators such as social sector expenditure-to-GDP, health and education spending ratios, and SDG tracking metrics are affected.

- Apparent improvements in these ratios (due to lower GDP) may mask real underinvestment in human capital.

- Example – National Health Policy Targets: Achieving 2.5% of GDP expenditure on health may appear closer numerically, but actual spending gaps persist.

3. Structural and Methodological Implications for Economic Governance

3.1 Improved Data Accuracy and Structural Representation

- The new series enhances realism by incorporating multi-activity enterprise segmentation, better coverage of LLPs, and use of high-frequency household sector data (ASUSE + PLFS).

- This leads to more accurate sectoral contributions, especially in manufacturing and informal sectors, improving policy targeting.

- Example – Manufacturing Growth Estimates: Strong real GVA growth (~9–12%) provides clearer signals for industrial policy interventions like Production Linked Incentive (PLI) schemes.

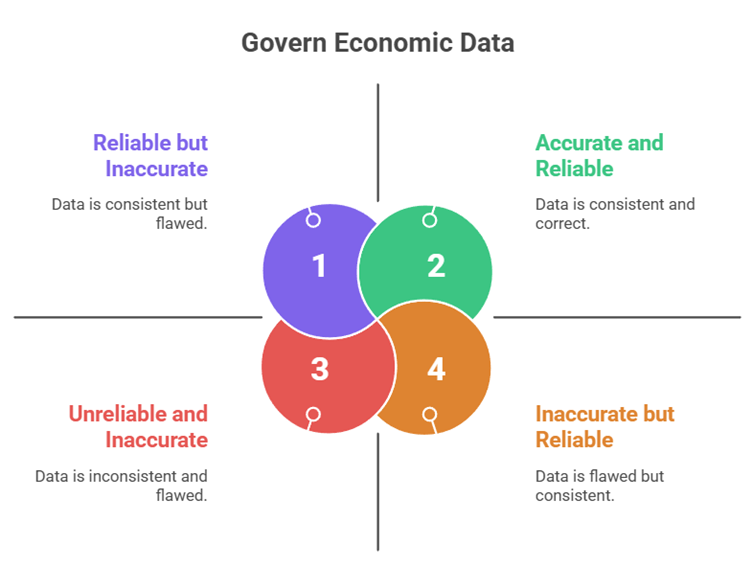

3.2 Challenges in Data Reliability and Volatility

- Dependence on survey-based estimates (ASUSE) introduces volatility in indicators such as Gross Value Added per Worker (GVAPW), affecting consistency.

- Fluctuations across years and states complicate trend analysis and long-term planning.

- Case Study – Bihar Manufacturing GVAPW Variations: Significant year-to-year swings highlight data instability, necessitating smoothing techniques like moving averages.

3.3 Need for Institutional and Statistical Reforms

- Limitations in datasets like Annual Survey of Industries (ASI) and challenges in allocating corporate GVA across states require reforms in statistical systems.

- Integration of GST, MCA databases, and adoption of rotating panel surveys can enhance robustness.

- Example – Digital Data Integration Initiatives: Leveraging GST analytics for regional economic estimation can improve accuracy of state-level GDP calculations.

Conclusion

- The downward revision of nominal GDP under the new base year reflects a methodologically superior and more realistic estimation framework, even though it temporarily worsens key fiscal ratios such as deficit and debt relative to GDP.

- While this may constrain fiscal optics and complicate short-term policy targets, it strengthens the credibility of macroeconomic data, which is crucial for long-term planning.

- Moving forward, improving statistical systems through better survey design, integration of administrative datasets like GST and MCA, and enhanced state-level estimation techniques will be essential.

- Coupled with sustained emphasis on fiscal discipline and quality expenditure, these reforms can ensure that India’s economic policymaking remains both data-driven and development-oriented.

Recap: