Impact of EU CBAM on India’s Carbon Market Design for Energy-Intensive Industries

EU CBAM impact on India carbon market has become a critical policy issue as global climate regulations reshape trade dynamics. The Carbon Border Adjustment Mechanism (CBAM) is a trade-linked climate policy tool introduced by the European Union (EU) to impose a carbon price on imports of carbon-intensive goods such as steel, cement, aluminium, fertilizers, electricity, and hydrogen, aligning them with the EU’s domestic Emissions Trading System (ETS).

It aims to prevent carbon leakage while incentivising cleaner production globally. For India—where energy-intensive industries like steel and cement account for nearly a quarter of total emissions—CBAM has emerged as a critical external driver shaping the evolution of a domestic carbon market framework, especially in the context of India’s net-zero 2070 commitment and expanding industrial decarbonisation strategies.

1. CBAM as an External Regulatory Pressure on India’s Carbon Market Design

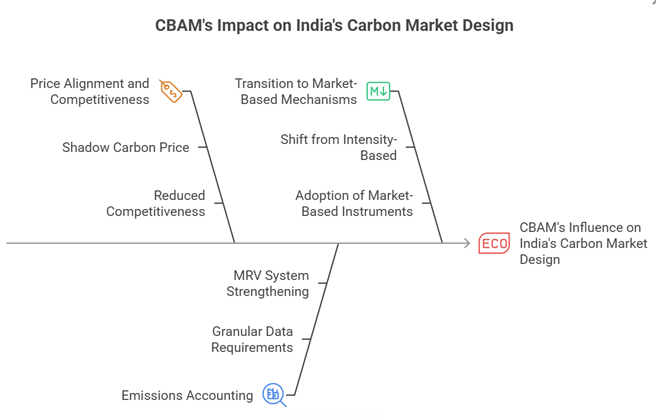

a) Price Alignment and Competitiveness Challenges

- CBAM effectively imposes a shadow carbon price on Indian exports entering the EU, exposing the absence of a comparable domestic carbon pricing mechanism in India.

- Indian industries, particularly steel and aluminium exporters, face the risk of reduced competitiveness unless emissions are priced domestically to offset CBAM liabilities.

- Example: Indian steel exports to the EU, which constitute a significant share of high-value exports, could face increased costs, compelling firms to adopt low-carbon technologies like green hydrogen-based steelmaking.

b) Push for Measurable and Verifiable Emissions Accounting

- CBAM requires granular, product-level emissions data, forcing India to strengthen its Monitoring, Reporting, and Verification (MRV) systems.

- This has accelerated policy efforts toward establishing a credible domestic carbon credit trading system, ensuring compatibility with global standards.

- Case Study: India’s Carbon Credit Trading Scheme (CCTS) under the Energy Conservation Act amendment reflects a shift toward measurable emissions frameworks in sectors like cement and power.

c) Transition from Intensity-Based to Market-Based Mechanisms

- India’s earlier approach, such as the Perform, Achieve and Trade (PAT) scheme, focused on energy efficiency targets rather than absolute emissions pricing.

- CBAM pressures India to transition toward market-based carbon pricing instruments, including cap-and-trade or hybrid models.

- Example: The gradual evolution of PAT into a broader carbon market signals a structural policy shift influenced by global mechanisms like CBAM.

2. Implications for Domestic Carbon Market Design in Energy-Intensive Sectors

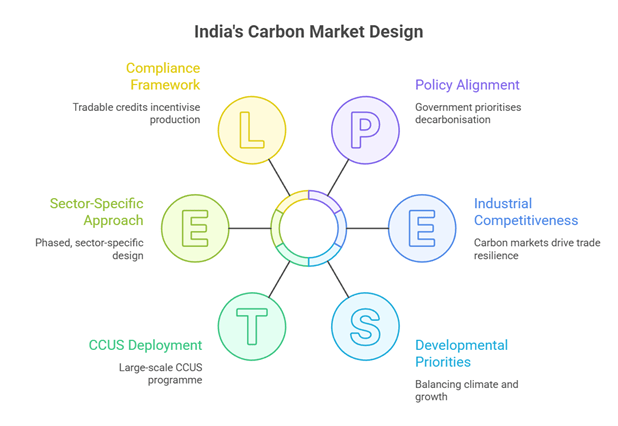

a) Focus on “Hard-to-Abate” Industrial Decarbonisation

- CBAM reinforces India’s prioritisation of hard-to-abate sectors such as steel, cement, refineries, and chemicals in its carbon market design.

- Policies are increasingly aligned with technologies like Carbon Capture, Utilization, and Storage (CCUS) to reduce process emissions.

- Case Study: The planned ₹20,000 crore CCUS programme aims at large-scale deployment in industrial clusters, targeting emissions from smokestacks rather than diffuse sources.

b) Integration of Carbon Markets with Industrial Policy

- Domestic carbon markets are being designed not just as environmental tools but as instruments of industrial competitiveness and trade resilience.

- Incentivising low-carbon production through tradable credits helps industries internalise carbon costs while maintaining export viability.

- Example: India’s push for Green Steel Mission and Production Linked Incentives (PLI) for clean technologies complements carbon market development.

c) Sector-Specific Calibration and Gradual Phasing

- Unlike the EU’s economy-wide ETS, India is adopting a phased, sector-specific approach, initially targeting energy-intensive industries.

- This calibrated design reflects concerns over economic growth, energy security, and employment, balancing climate goals with developmental priorities.

- Case Study: Pilot carbon trading mechanisms in the power and industrial sectors are being tested before full-scale implementation.

3. Opportunities, Constraints, and Strategic Responses

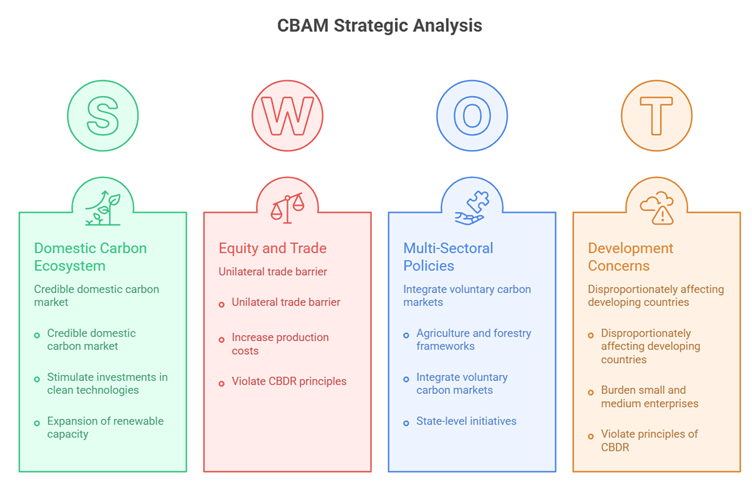

a) Opportunity to Build a Robust Domestic Carbon Ecosystem

- CBAM provides an opportunity to create a credible domestic carbon market, reducing dependence on external compliance mechanisms.

- It can stimulate investments in clean technologies, renewable energy, and energy efficiency, aligning with India’s climate commitments.

- Example: Expansion of renewable capacity and green hydrogen initiatives can generate tradable carbon credits domestically.

b) Constraints: Equity, Trade Fairness, and Development Concerns

- CBAM has been criticised as a unilateral trade barrier, disproportionately affecting developing countries with lower historical emissions.

- India faces challenges in ensuring that carbon pricing does not increase production costs or burden small and medium enterprises.

- Case Study: India has raised concerns at multilateral forums, arguing that CBAM may violate principles of Common But Differentiated Responsibilities (CBDR).

c) Need for Multi-Sectoral and Complementary Policies

- While industrial carbon markets are evolving, sectors like agriculture and forestry require separate frameworks such as Carbon Dioxide Removal (CDR) and nature-based solutions.

- Integrating voluntary carbon markets with compliance markets can enhance overall effectiveness.

- Example: State-level initiatives promoting soil carbon sequestration and agroforestry demonstrate parallel pathways for carbon credit generation outside industrial sectors.

Conclusion

The EU’s CBAM has acted as a powerful external catalyst, accelerating India’s transition from fragmented, intensity-based mechanisms to a more integrated, market-driven carbon pricing architecture for energy-intensive industries. While it poses short-term competitiveness challenges, it also offers a strategic opportunity to modernise industrial systems and embed low-carbon pathways into economic growth.

Going forward, India must adopt a balanced approach—strengthening domestic carbon markets, investing in technologies like CCUS and green hydrogen, and ensuring policy coherence across sectors—while safeguarding developmental priorities.

A well-designed, transparent, and globally aligned carbon market could not only mitigate CBAM impacts but also position India as a leader in the emerging low-carbon global economy.

Recap: